Journal Entries

Terms

Adjusting Entries

Closing Entries

Bank Reconciliation

100

Record the journal entry:

SCL issued 10,000 common shares in exchange for $250,000 cash.

Dr Cash 250,000

Cr Common Shares 250,000

100

An element of the fundamental qualitative characteristic of relevance that states that accounting information is relevant to decision makers when it helps predict future outcomes.

Predictive Value

100

Record the adjusting entry: The deposits of $3,400 from customers were for future services and were recorded as unearned revenue. As at December 31, three-quarters of these services had been provided.

Dr Unearned Revenue 2,550

Cr Service Revenue 2,550

100

Record the closing entry for the revenues:

Sales Revenue $34,000

Unearned Revenue $2,000

COGS $17,000

Dr Sales Revenue 34,000

Cr Income Summary 34,000

100

Outstanding cheques

Do these affect the bank or book side?

Do we add or deduct?

Outstanding cheques are deducted on the bank side.

200

Record the journal entry: WIL paid $1,800 cash for a one-year insurance policy covering the new equipment for the period January 1 to December 31.

Dr Prepaid Insurance 1,800

Cr Cash 1,800

200

An enhancing qualitative characteristic that states that the information in financial statements must be timely to be useful.

Timeliness

200

Record the adjusting entry:

There is $2,000 in wages owed at year end.

Dr Wages Expense

Cr Wages Payable

200

Record the closing entry for the following expenses:

Cost of goods sold 130,000

Wages Expense 34,000

Repairs and Maint exp 25,000

Miscellaneous exp 15,000

Dr Income Summary 204,000

Cr Cost of goods sold 130,000

Cr Wages Expense 34,000

Cr Repairs and Maint exp 25,000

Cr Miscellaneous exp 15,000

200

NSF Cheques

Do these affect the bank or book side?

Do we add or deduct?

NSF cheques are deducted on the book side

300

Record the journal entry: Clearly Corp. sold products to customers for $34,000, of which $21,000 was received in cash and the balance was on account. SCL's customers will pay at a later date. The products that were sold had cost SCL $17,000.

Dr Cash 21,000

Dr A/R 13,000

Cr Sales 34,000

Dr COGS 17,000

Cr Inventory 17,000

300

A profitability measure (ratio) that compares a company's gross profit to its total revenues. It measures what portion of each sales dollar is left after covering COGS.

Gross Profit (Margin) Ratio

300

Record the adjusting entry:

A count of the supplies at year end revealed that $500 of the $5,000 supplies were still on hand.

Dr Supplies Expense $4,500

Cr Supplies $4,500

300

Record the entry to close the $3,400 dividends declared account.

Dr Retained Earnings 3,400

Cr Dividends Declared 3,400

300

The bookkeeper incorrectly recorded a cheque for supplies $150 when the correct amount was $510. Where should this error be corrected- bank/book side?

How much is the correction? Deduct or Add?

Book

Deduct $360

400

Record the journal entry: Dividends in the amount of $400 were declared by SCL's board of directors and paid.

Dr Dividends Declared 400

Cr Cash 400

400

A company cash flow pattern like this:

Operating Investing Financing

+ + +suggests what about the company's success?

Successful, but actively repositioning or relocating using financing from operations together with cash from creditors and shareholders

400

Record the adjusting entry for the year:

A building was purchased on January 1st for $120,000. The building is being depreciated over 20 years with a residual value of $20,000. The company's year end is December 31st.

Dr Depreciation Expense 5,000

Cr Accumulated Depreciation 5,000

400

Calculate the balance in the income summary account after closing revenues and expenses

$343,000

400

What is the AFDA amount on the company's balance sheet?

$42,000

500

Record the journal entry: Flip Corp. received $3,200 for services to be provided to customers in the upcoming 4 months.

Dr Cash 3,200

Cr Unearned Revenue 3,200

500

The set of policies and procedures established by an enterprise to safeguard its assets and ensure the integrity of its accounting system.

Internal control system

500

Record the adjusting entry:

Income tax payable of 30% on net income of $100,000 is owed.

Dr Income tax expense 30,000

Cr Income tax payable 30,000

500

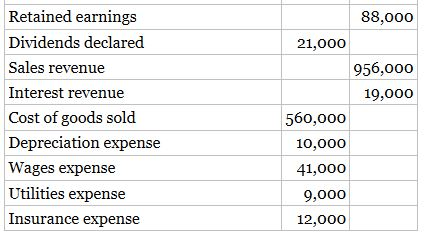

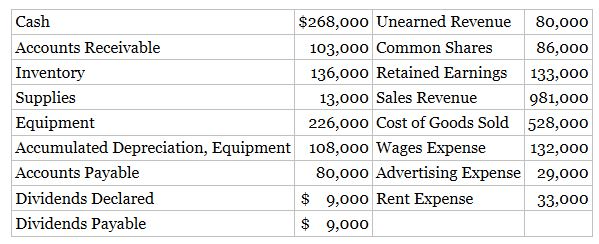

Record the ending balance in retained earnings after all the closing entries have been recorded.

Begin RE 133,000 + Sales 981,000 - COGS 528,000 - Wages Expense 132,000 - Advertising Expense 29,000- Rent Expense 33,000- Divs 9,000

= $383,000

500

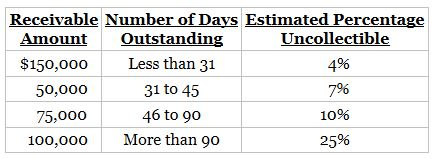

The company has a $5,000 debit balance in AFDA at December 31st, they determine based on the allowance aging analysis that the ending balance should be $45,000. What entry is required?

Dr Bad debt expense 50,000

Cr AFDA 50,000