Basic Economic Thinking

Supply & Demand

Production & Costs

Graph it!

AP-Level Reasoning

100

This is the value of the next best alternative forgone.

What is opportunity cost?

100

The price at which quantity supplied equals quantity demanded.

What is equilibrium price?

100

Total revenue minus total cost equals this.

What is profit?

100

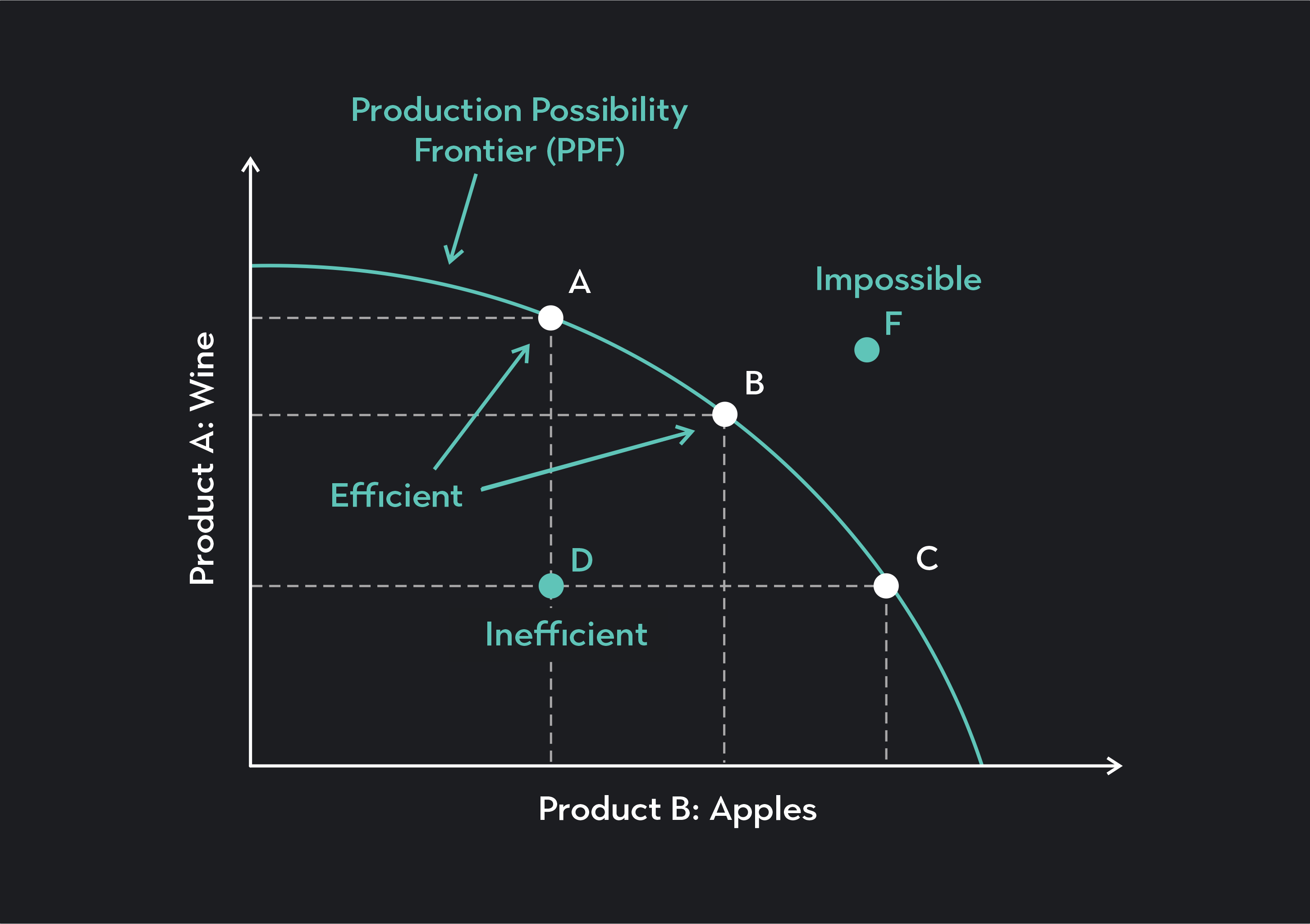

What is a production possibilities curve?

100

Why do economists assume people respond to incentives?

What is to predict rational behavior?

200

This type of statement describes what ought to be.

What is a normative statement?

200

An increase in consumer income for a normal good causes this change.

What is an increase in demand?

200

The law that explains why marginal product eventually falls.

What is the law of diminishing marginal returns?

200

Show an increase in demand for a product.

What is a rightward shift of demand?

200

Why does MC intersect ATC at its lowest point?

What is MC pulls averages?

300

When all resources are fully and efficiently used, the economy is operating here.

This type of statement describes what ought to be.

300

A tax on sellers causes the supply curve to do this.

What is shift left?

300

The cost that does not change with output in the short run.

What is fixed cost?

300

Graph a per-unit tax on producers.

What is an upward/leftward shift of supply?

300

Why does a price ceiling cause shortages?

What is quantity demanded exceeds quantity supplied?

400

This PPC concept explains why the curve is bowed outward.

What is increasing opportunity cost?

400

If demand increases and supply decreases, this will definitely happen to price.

What is an increase?

400

A firm should shut down in the short run when price is below this.

What is average variable cost (AVC)?

400

Draw ATC, AVC, and MC and show the profit-maximizing output

What is where MR = MC?

400

Why is supply more elastic in the long run?

What is firms have time to adjust inputs?

500

A government subsidy lowers costs for producers. This is an example of what?

What is an incentive?

500

This concept explains how much quantity demanded responds to a price change.

What is price elasticity of demand?

500

In perfect competition, this equals demand, average revenue, and marginal revenue.

What is price?

500

Graph a firm earning an economic loss but continuing to produce.

What is P < ATC but P ≥ AVC?

500

Explain why a firm may operate at a loss in the short run but exit in the long run.

What is because firms can cover variable costs but not total costs?