Unit 1 Basics Economics

Unit 2 Supply, Demand, and Consumer Choice

Unit 3 Costs of production and perfect competition

More

Perfect Competition

Perfect Competition

More Production Costs

100

The study that focuses on firms, households, and individuals is known as

What is microeconomics?

100

In order to have Demand, these two aspects must exist for a Consumer

What is Willing and Able

100

market in which buyers and sellers are numerous and well informed that all elements of monopoly are absent.

What is perfect competition?

100

MR=D=AR=P stands for

What is Marginal Revenue, Demand, Average Revenue and Price

100

The formula for Total Costs

What is FC + VC

200

"Other things being equal."

What is Ceteris Paribus?

200

The point where the demand and supply curve intersect

Market Equilibrium

200

Long Run Profit is what kind of Efficiency

What is Allocative and Productive

200

Firms do these two things in the Long Run

What is Enter or Exit the Market?

200

As you add more of a variable input to a fixed input, the addtl output you get will eventually decrease is known as

what is the Law of Diminishing Marginal Utility

300

An economic system where the government has total control

What is Command Economy?

300

The relationship between Price and Qty on the Demand Curve

What is inverse

300

The Marginal Cost Curve Above Min AVC

What is PC Supply Curve?

300

The Market that most approximates a Perfectly Competitive Industry

What is Agriculture

300

The cost advantages that arise when a company increases its production volume leading to lower average costs per unit

What are Economies of Scale

400

Land, Labor, Capital, and entrepreneurship is also known as the...

What is the four factors of production

400

the Cross-Price Elasticity of these two goods is negative

What are Complement Goods?

400

Short run shutdown rule

Long run exit rule

P<AVC

400

The fall in total surplus that results from a market distortion, such as a tax, and is a loss of economic efficiency

What is Deadweight

400

What kind of profit is calculated when we subtract both Implicit and Explicit Costs from TR?

What is Economic Profit?

500

As the production of one good increases, producers must sacrifice ever-increasing amounts of the other goods because factors of production are not perfectly interchangeable between the production of both goods

What is Law of Increasing Opportunity Costs?

500

The Elasticity of Demand = 1

What is Unit Elastic?

500

A tax that is a fixed amount, no matter the change

What is a lump sum tax

500

The Socially Optimal Price is _____ on a Perfect Competition graph

P=MC

500

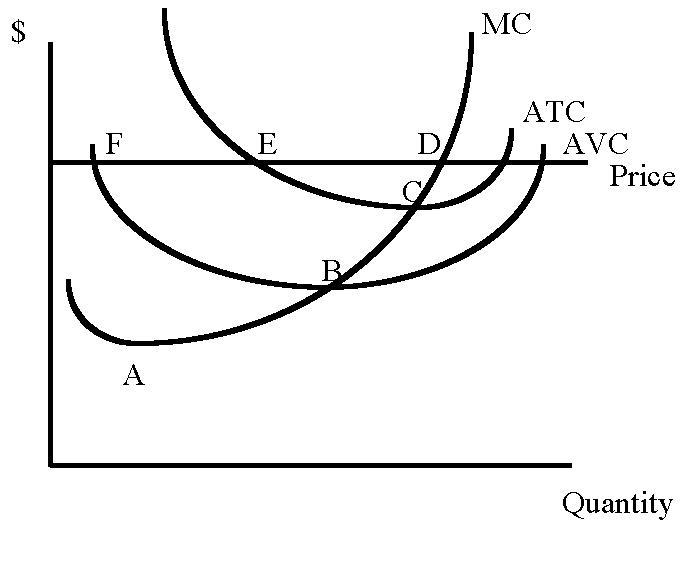

The Long Run Point on the graph as shown is

What is Point C?