Basic Concepts

Costs

Elasticity & Factor Market

Market Structures

Miscellaneous

Graphs

100

What is allocative efficiency?

When P = MC

100

The extra cost of producing one more unit of output.

What is marginal cost?

100

The change in total revenue resulting from the use of each additional unit of a resource.

What is marginal revenue product?

100

Large number of firms, standardized product, price takers, free entry and exit.

What is characteristics of purely (perfectly) competitive markets?

100

A strategy in which one firm's product is distinguished from competing products by means of its design, related services, quality, location, or other attributes.

What is product differentiation?

100

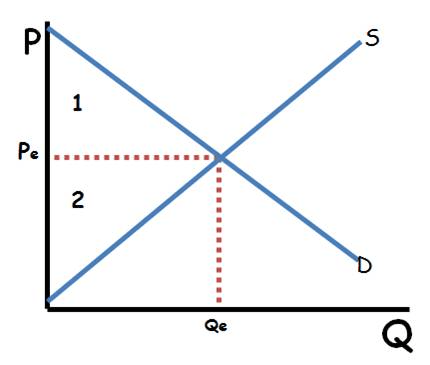

What is area 1 depicting?

Consumer Surplus

200

What is profit maximizing rule for all firms?

MR = MC

200

The monetary income a firm sacrifices when it uses a resource it owns rather than supplying the resource in the market.

Input costs that do not require an outlay of money by the firm.

What is implicit cost?

200

Cheese and bread are complementary goods, and the price of cheese has increased.

What happens to the demand for bread as a result?

If the price of cheese increases, the price for bread increases and the demand for bread decreases.

200

A perfectly competitive firm does this when their P>AVC but less than ATC.

What is continue to produce in the Short Run to minimize losses?

200

A good or service that is characterized by non-rivalry and non excludability.

What is a public good?

200

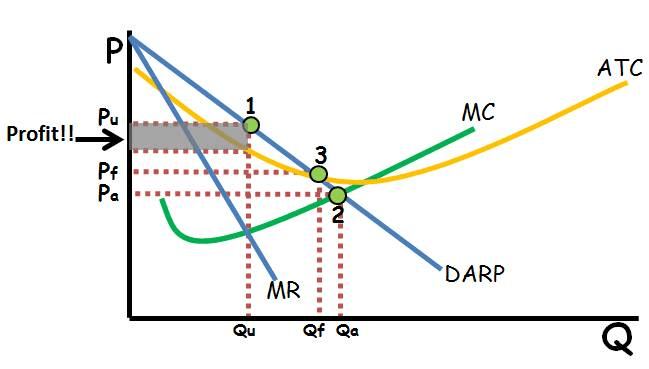

What type of graph is shown below?

A monopoly making positive profit (in the long run)

300

This graph highlights the possible combinations of products/output one individual can do in a given period of time.

What is Production Possibilities Frontier

300

The amount of other products that must be given forgone or sacrificed to produce a unit of a product.

What is opportunity cost?

300

The demand for a product is elastic and a monopoly decides to increase the price of their item. What happens to the firm's total revenue?

If demand is elastic, when price goes up, total revenue goes down.

300

Economies of scale, patents, control of key resources, non-price competition.

What is barriers to entry?

300

The inability of a market to bring about the allocation of resources that best satisfies the wants of society.

What is a market failure?

300

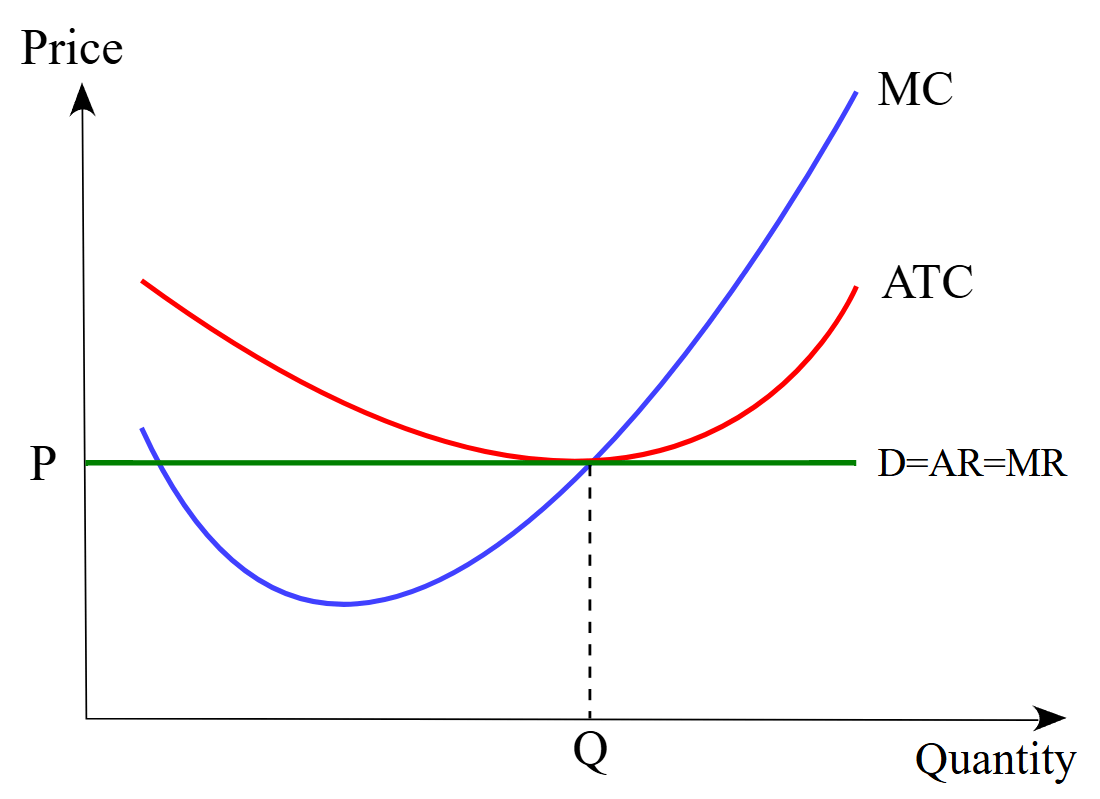

This perfect competition graph represents profit maximization in the...

What is the Long Run.

400

Reductions in combined consumer and producer surplus caused by an under allocation or overallocation of resources to the production of a good or service.

(Brings us away from our equilibrium)

What is dead weight loss (efficiency loss)

400

Any cost that in total does not change when the firm changes its output.

What is fixed costs?

400

What are the four factors of production?

Land, Labor, Capital and Entrepreneurship

400

A situation in which a change in price strategy (or some other strategy) by one firm will affect the sales and profits of another firm (or other firms).

What is mutual interdependence?

400

On a monopolistic graph, when the MR = 0, is the demand elastic, inelastic or unit elastic?

What is unit elastic?

400

Would the monopolistic firm shown in the graph below be making positive, negative, or zero economic profit?

What is Zero economic profit?

500

The price paid for the use of land, and other resources which are fixed in supply.

What is economic rent?

500

A firm's monetary payments to those who supply labor services, fuel, transportation services, etc.

What is explicit costs?

500

Assume the cross-price elasticity of demand between AirCab's flights and Good L is +1.4.

a. If the price of Good L decreases by 2%, by how much will the quantity of AirCab flights change?

b. Are AirCab's flights and Good L substitute, complement, or inferior goods? Explain why.

a. The quantity of AirCab's flights will decrease by 2.8%.

b. They are substitutes because as price decreases for Good L, the quantity demanded would increase, which would be a negative elasticity and if they are substitutes then the quantity demanded of a substitute would decrease, leading to a positive cross-price elasticity.

500

The selling of a product to different buyers at different prices when the price differences are not justified by differences in cost.

What is price discrimination?

500

The principle that as successive increments of a variable resource are added to a fixed resource, the marginal product of the variable resource will eventually decrease.

What is law of diminishing returns?

500

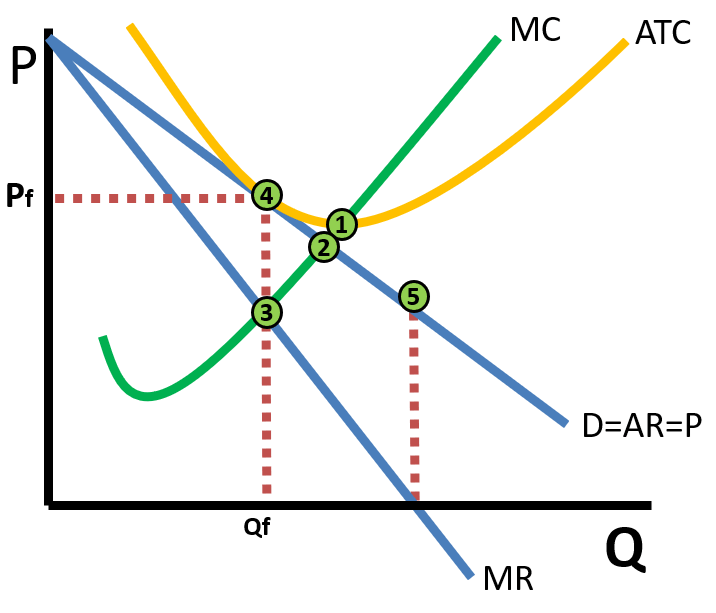

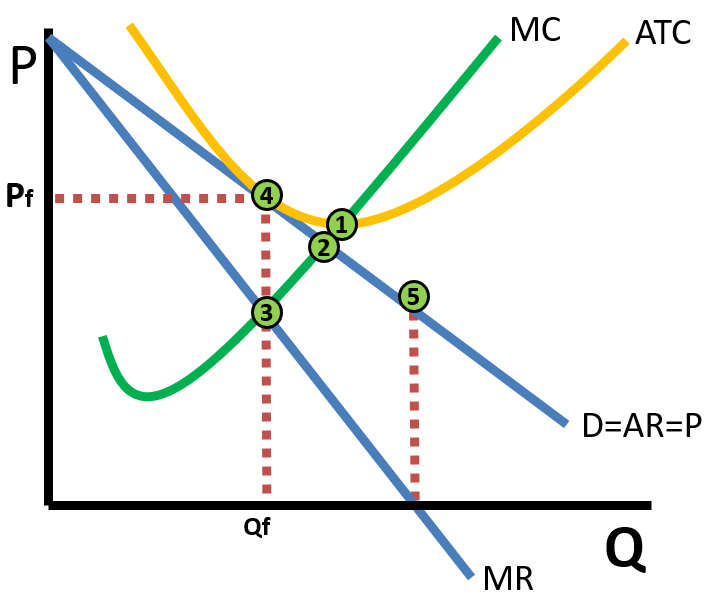

What does point 2 signify?

What does point 5 signify?

point 2 is the allocatively efficient quantity and price (socially optimal... best for society) where demand equals the Marginal Cost.

point 5 is the point of unit elasticity. The demand is inelastic to the right of the point and elastic to the left of the point.