Chapter 1a

Chapter1b

Chapter1c

Chapter1d

Chapter1e

100

An enterprise which strives to achieve its objectives; be they to be profitable (for profit) or otherwise (non-profit), through the provision of either tangible items (goods) or intangible offerings (services) or a combination of both to its customers.

What is a Business?

100

potential to lose resources such as time and money or otherwise not be able to accomplish an organization's goal.

What is risk?

100

the resources which business require to function effectively.

What is Factors of production?

100

List the four types of Economic Systems

1. Capitalism

2. Communism

3. Socialism

4. Mixed Economy

100

a decline in gross domestic product that lasts for two (2) or more consecutive quarters.

What is Recession?

200

a measurement of the output of goods and services people can buy with the money they have.

What is Standard of living?

200

the money a company receives by providing deliverables (be they goods or services) to customers

What is revenue?

200

The combination of policies, laws and choices made by a nation's government to establish the systems that determine what goods and services are produced and how they are allocated.

What is Economic System?

200

an economic system characterised by private ownership in which the free market alone controls the production of goods and services. This is based on competition in the marketplace and private ownership of the factors of production.

What is capitalism?

200

a government’s programs for controlling the amount of money circulating in the economy and interest rates. Changes in the money supply affect both the level of economic activity and the rate of inflation.

What is a Monetary Policy?

300

the general level of human happiness based on life expectancy, education standards, health, sanitation and leisure time.

What is Quality of Life?

300

expenses such as rent, salaries, supplies, transportation and many other items that a company incurs from the provision of its deliverables.

What is costs?

300

The study of how a society uses scarce resources to produce and to distribute deliverables.

What is Economics?

300

a system of social organization in which all property is owned by the community and each person contributes and receives according to their ability and needs. The government owns virtually all resources and controls all markets thereby resulting in the economic decision-making being centralized.

What is Communism?

300

this policy uses government spending and tax policies to influence macroeconomic conditions, including aggregate demand, employment, and inflation.

What is Fiscal Policy?

400

Name the four traditional factors of production?

1. Natural Resources

2. Labour (Human Resources)

3. Capital

4. Entrepreneurship

400

Name the four sectors that comprised the internal environment.

What is..

1. Entrepreneurs

2. Managers

3. Workers

4. Customers

400

an economic theory of social organization which advocates that the means of production, distribution, and exchange should be owned or regulated by the community as a whole. A socialist state controls critical, large-scale industries such as transportation, communications, and utilities. Smaller businesses and those considered less critical, such as retail, may be privately owned.

What is Socialism?

400

an economic system which protects the private property and allows a level of economic freedom in the use of capital, but also allows for governments to interfere in economic activities in order to achieve social aims. Mixed economies use more than one (1) economic system. Through policies and laws, the government transfers money to the poor, the unemployed and the elderly or disabled. To protect smaller firms and entrepreneurs, the government has passed legislation that requires that the large corporations compete fairly against weaker competitors.

What is a Mixed Economy?

400

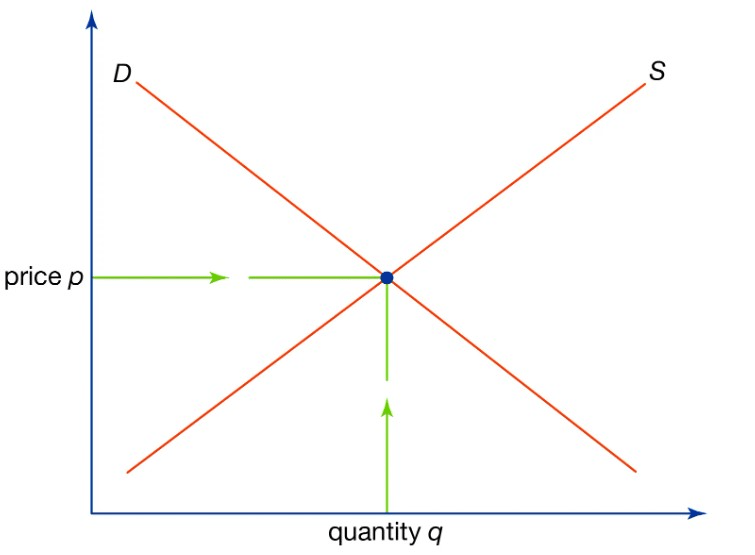

Explain the graph.

the quantity of a good or service that people are willing to buy at various prices. The higher the price, the lower the quantity demanded, and vice versa

500

Name the six factors of production which includes the traditional and the new age factors.

1. Natural Resources

2. Labour (human resources)

3. Capital

4. Entrepreneurship

5. Knowledge

6. Skills

500

Name the at least five sectors in the External Environment.

What is ...

1. Economic

2. Political/Legal

3. Demographic

4. Social

5. Competitive

6. Global

7. Technological

500

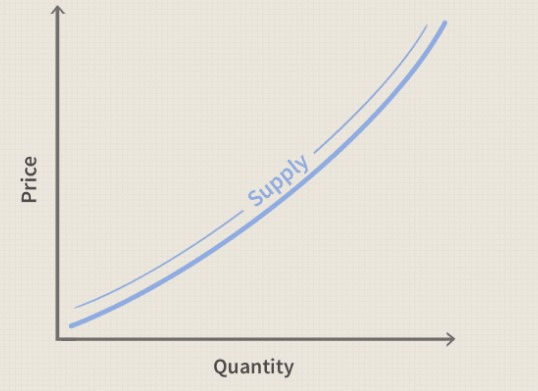

Explain the graph

the quantity of a good or service that businesses will make available at various prices. The higher the price, the greater the number of goods or services a supplier will supply and vice versa.

500

What is the point of intersection called and mean?

What is point of equilibrium? This means that the quantity demanded equals the quantity supplied at the agreed price.

500

What happens to the demand curve if the buyer's income increase?

What is a shift to the right? It shifts the demand curve to the right.