Revenue Recognition

Cash & Receivables

Investments

PP&E

Depreciation, Impairment & Disposition

100

The first step in the revenue recognition process under IFRS is

a) determine the transaction price.

b) identify the separate performance obligations of the contract.

c) identify the contract with customers.

d) allocate the transaction price to the separate performance obligations.

c

100

Grieves Company has the following items at year end:

Grieves should report cash and cash equivalents of

$42,000 + $1,500 + $6,500 = $50,000

100

awkeye Ltd. holds equities securities in its portfolio and is accounting for those investments using the FV-NI method. On March 1, 2023, the company purchased 10,000 shares of a publicly traded company for $2,500,000 and paid a commission (brokerage fee) of $2,500 on the purchase transaction. What is the cost base of the investment to include for the recording of the portfolio value?

$2,500,000

100

Grappa Grapes is a privately held winery. The following is a partial list of the items Grappa has at its December 31 year end:

What value should be assigned to the productive biological assets on the balance sheet on December 31?

$825,000 = $75,000 + $750,000

100

Depreciation commences or continues when

a) the asset has been paid for.

b) the asset is available for use.

c) the asset’s fair value can be recovered.

d) the asset is taken out of service.

b.

200

On January 1, 2023, Milton Ltd. sold land that cost $180,000 for $240,000, receiving a note bearing interest at 10 percent. The note will be paid in three annual instalments of $96,510 starting December 31, 2023. Assuming that collection of the note is very uncertain, how much revenue from this sale should Milton recognize in 2023?

a) $0

b) $18,000

c) $24,000

d) $96,510

a

200

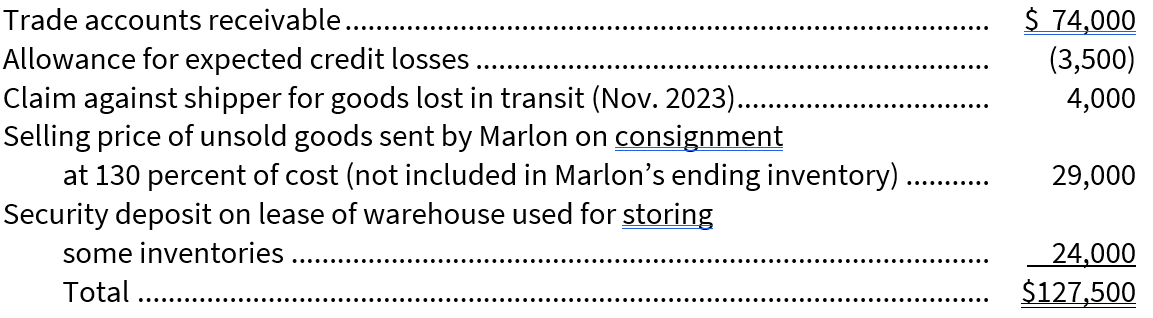

On Marlon Corp.’s December 31, 2023 statement of financial position, the current receivables consisted of the following:

At December 31, 2023, the correct total of Marlon’s current net receivables was:

$74,500

200

On its December 31, 2023, balance sheet, Red Corp. reported a short-term investment in equity securities, under the fair value through net income model, at $330,000. At December 31, 2024, the fair value of the securities was $350,000. What should Red report on its 2024 income statement as a result of the increase in fair value of the investments during 2024?

investment income of $20,000

200

On January 2, 2023, Holliwell Inc. replaced its boiler with a more efficient one. The following information was available on that date:

The old boiler was sold for $2,400. At what amount should Holliwell capitalize the cost of the new boiler?

$36,000 + $3,200 = $39,200

200

Sage Corp is a publicly traded company that has just purchased a new piece of equipment for its production process. The equipment costs $50,000 with an $8,000 residual value, an estimated useful life of 7 years and an expected life of 10 years with a $2,000 salvage value. Assuming that Sage has a December 31 year end and the equipment was purchased on January 1, how much depreciation expense should the company record at the end of year one? The company uses the straight-line method.

($50,000 – $8,000)/7 years =$6,000

300

Lonestar Deals sells household furniture and appliances. The manager decided to sell a couch to a customer at a75% discount with 9 months to pay, no interest and no deposit, because the couch was no longer in style and had been sitting in the back of the warehouse for over 2 years. Normally, the maximum discount is 10% and customers are never given more than 30 days to pay. The final sale price of the couch was $500. What would be the appropriate journal entry when the customer picks up the couch?

No Entry

300

The following information is available for Pirate Company:

As a result of a review and aging of Accounts Receivable in early January 2025, it was determined that an Allowance for Expected Credit Losses balance of $7,500 is required at December 31, 2024. What amount should Pirate record as loss on impairment for calendar 2024?

$7,000 – $2,800 = $4,200 unadjusted credit balance

$4,200 – $7,500 desired balance = $3,300 loss on impairment

300

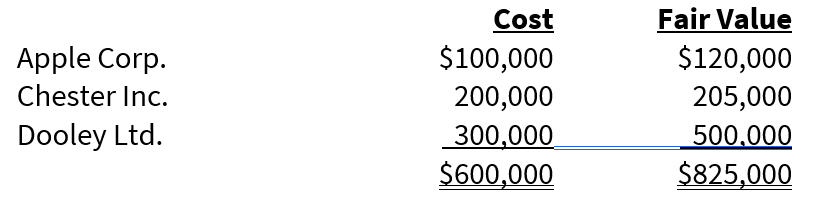

At December 31, 2023, Swift Current Inc. has the following portfolio of common shares in which it does not have significant influence:

Assuming Swift Current uses the fair value through other comprehensive income (FV-OCI) model to account for this portfolio of investments, the most informative entry to record the year-end adjustment is:

300

Chad Corporation purchased a tract of land for $765,000, which included a warehouse and office building. The following data were collected concerning the property:

What are the appropriate amounts that Chad should record for the land, warehouse, and office building, respectively?

land, $255,000; warehouse, $170,000; office building, $340,000

300

Monkey Shines Ltd., a Canadian public corporation, owns equipment for which the following year-end information is available:

The recoverable amount to be used in the determination of impairment is:

b. higher of value in use and FV less disposal costs

400

Builder Bob Construction Inc. began work on a $7,500,000 non-cancellable contract in 2023 to construct a retail building. During 2023, Builder Bob incurred costs of $1,500,000 and billed its customers for $1,400,000 (non-refundable) and collected $1,000,000. At December 31, 2023, the estimated future costs to complete the project total $2,500,000. What is the construction expense, assuming Builder Bob is using the percentage-of-completion method?

$1,500,000

400

At year end, Gold Sky Inc. started the process to review its $3,500,000 of accounts receivable to estimate what amount outstanding could potentially be returned by the customer. There was a recent memo from the production manager that stated a process error was found in one of the assembly lines, potentially causing a defect in the output. As a result, a significant amount of product is expected to be returned. Assuming a 15% estimated return rate, what would be the entry to journalize this under IFRS?

400

On January 1, 2023, Mack Co. purchased a 5-year, 8% bond with a face value of $200,000. The purchase price of $184,556 was consistent with a 10% yield. Interest is payable semi-annually on January 1 and July 1. The bonds mature on January 1, 2028. The amortized cost of the bond on the maturity date is:

$200,000

400

Mozambique Ltd. received a $250,000 grant from the federal government to help buy equipment as an incentive for them to establish manufacturing operations in Ottawa. The company assumes the equipment has a 10-year useful life and uses straight-line depreciation. If Mozambique uses the cost reduction method for such transactions, it should record this transaction as a:

a) memo entry only.

b) credit to Equipment for $250,000.

c) credit to Deferred Revenue for $250,000.

d) credit to Contribution Revenue for $250,000.

b) credit to Equipment for $250,000.

400

Ash Industries has several assets as part of a cash-generating unit that have limited use due to changing market trends and declining demand for the product produced by these assets. Management estimates that the carrying value of these assets is $85,000 and the assets have no other use. The company intends on producing this product for three more years prior to disposing of the assets. The net future cash flows related to the product production and sale of the equipment is $87,500, while the present value of the cash flows is $81,750. The fair value less the cost of disposal of the assets is estimated at $71,000. What is the value of the impairment loss under the rational entity model?

b. $85,000 – $81,750 = $3,250

500

Hemsworth Ltd. began work in 2023 on a contract for $960,000. Other details follow:

Assume that Hemsworth uses the percentage-of-completion method of accounting. The portion of the total gross profit to be recognized in 2023 is

$80,000

500

During the year, Popsicle Inc., which uses the allowance method, made an entry to write off a $4,000 uncollectible account. Before this entry was posted, the balance in accounts receivable was $80,000 and the balance in the allowance account was $7,000. The net realizable value of accounts receivable after the write-off entry was:

($80,000 – $4,000) – ($7,000 – $4,000) = $73,000

500

On July 1, 2023, Harry Ltd. purchased $200,000 (par value) of Prince’s 8% bonds. Because the market rate was 9%, Harry purchased them for $186,992. The bonds pay interest semi-annually on December 31 and June 30. Harry uses the amortized cost model and the effective interest method to recognize interest income on bond investments.

Rounding values to the nearest dollar (if necessary), the entry to recognize receipt of the first interest payment on December 31, 2023 will include a

a) debit to Cash of $9,000.

b) credit to Interest Income of $8,415.

c) debit to Cash of $8,415.

d) credit to Interest Income of $8,000.

b. Interest income = $186,992 x 9% x 6 ÷ 12 = $8,415 rounded

500

Bally Ho Inc. traded one of its used trailers (cost $15,000, accumulated depreciation $13,500) for another used trailer with a fair value of $2,400. Bally Ho also paid $300 to complete the transaction. Since the exchange will leave Bally Ho in the same economic position, this transaction lacks commercial substance. What is the gain or loss on the exchange?

$0 (no gain or loss)

500

The following information is available for an asset that is classified as held for sale:

If the asset were sold on April 1, 2023 for $27,600, there would be

$27,600 – ($50,000 – $24,300) = $1,900 gain