FHA

Conventional

VA

USDA

DPA

100

If the credit report utilized by TOTAL Mortgage Scorecard indicates that the Borrower has $_________ or more collectively in Disputed Derogatory Credit Accounts, the Mortgage must be downgraded to a Refer and manually underwritten.

$1,000.00

100

True or False

All conventional loans require a minimum of 3 tradeline for the previous 12 months and 2 tradelines for the previous 24 months ON TIME PAYMENTS.

FALSE.

Conventional loans have NO tradeline requirements.

100

What 2 documents show's if the borrower is eligible for VA benefits?

DD214 & COE (Certificate of Eligibility)

100

A borrower wants to purchase their 2nd home in a rural area (Ocala,FL) - but has a credit score of 680. Can the borrower purchase this home as a USDA loan?

NO! USDA loans are only for primary residences.

100

Minimum Credit Score for DPA loan?

640

200

Judgements (TOTAL)

The Mortgagee must verify that court-ordered Judgments are resolved or paid off prior to or at closing. There is no exceptions or exclusions to this guideline.

TRUE OR FALSE? Why?

FALSE.

A Judgment is considered resolved if the Borrower has entered into a valid agreement with the creditor to make regular payments on the debt, the Borrower has made timely payments for at least three months of scheduled payments and the Judgment will not supersede the FHA-insured mortgage lien. The cannot prepay scheduled payments in order to meet the required minimum of three months of payments. The Mortgagee must include the payment amount in the agreement in the Borrower’s monthly liabilities and debt. The Mortgagee must obtain a copy of the agreement and evidence that payments were made on time in accordance with the agreement. Borrower

200

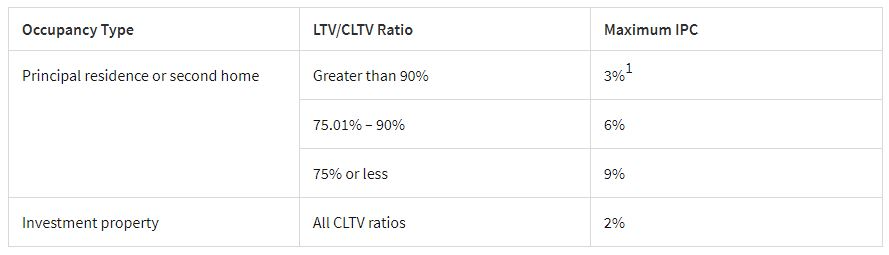

What is the maximum seller credit based on the LTV (Principal residence or second home

75.01% – 90% LTV)?

6%

200

Is the funding fee always required on VA Loans?

NO. DISABLED VETS CAN BE EXEMPT FROM THE FUNDING FEE AND PROPERTY TAXES!

200

What is the minimum credit score for USDA?

The USDA does not set a minimum credit score requirement, but most lenders require a score of at least 640, which is the minimum score needed to qualify for automatic approval using the USDA's Guaranteed Underwriting System (GUS). GUS is the USDA's automated underwriting system, which automates the process of credit risk evaluation.

It is possible to qualify with a score below 640 with some lenders, but those files require manual underwriting. Even people without a credit score at all can sometimes qualify, though there are other income and financial requirements they must meet.

Credit guidelines can vary by lender and other factors.

200

Is there an income limit max for DPA loans? If so how can you check the limits?

YES! Go to the DPA provider's website and look up the guidelines.

300

Bankruptcy (TOTAL)

The Mortgagee must document the passage of ________ years since the discharge date of a Chapter 7 bankruptcy.

The Mortgagee must document the passage of ________ years since the discharge date of a Chapter 13 bankruptcy.

Chapter 7: All borrowers must wait least two years after the discharge date of a Chapter 7 Bankruptcy. The discharge date should not be confused with the date bankruptcy was filed.

Chapter 13: FHA rules allow a lender to consider approving an FHA loan application from a borrower who is still paying on a Chapter 13 Bankruptcy-but only if those payments have been made and verified for a period of at least one year.

300

Length of Self-Employment

(TRUE OR FALSE)

If a borrower has been self employed for less than 2 years and provide the most recent signed federal income tax returns to show the borrower has been in the same line of work - Can we consider this as effective income?

TRUE!

Fannie Mae generally requires lenders to obtain a two-year history of the borrower’s prior earnings as a means of demonstrating the likelihood that the income will continue to be received.

However, a person who has a shorter history of self-employment — 12 to 24 months — may be considered, as long as the borrower’s most recent signed federal income tax returns reflect the receipt of such income as the same (or greater) level in a field that provides the same products or services as the current business or in an occupation in which he or she had similar responsibilities to those undertaken in connection with the current business. In such cases, the lender must give careful consideration to the nature of the borrower’s level of experience, and the amount of debt the business has acquired.

300

Minimum Service Required

(TRUE OR FALSE)

Living Veterans MUST be on the mortgage application with spouse in order for the VA benefits to be applied.

FALSE!! There is no time requirement. Veteran must have died on active duty or from a service-connected disability

300

Can you name 5 NON- TRADITIONAL tradelines that USDA approves?

- Rent

- Utility bills

- Insurance

- Childcare

- Medical bills

- Car lease

- Personal loan

- School tuition

- Cell phone bills

300

Are ALL applicants required to be first-time home buyers to get the DPA benefit?

NO!

Only 1 borrower must be a FTHB.

400

Foreclosure (TOTAL)

The Mortgagee must manually downgrade to a Refer if the Borrower had a foreclosure in which title transferred from the Borrower within ______ years of case number assignment.

3 Years.

If the credit report does not verify the date of the transfer of title through the foreclosure, the Mortgagee must obtain the foreclosure documents.

400

Can a borrower use their business bank statements as effective income to purchase their PRIMARY residence?

YES!

VERY IMPORTANT: DO NOT UPLOAD BUSINESS BANK STATEMENTS INTO ENCOMPASS. ONLY PERSONAL AND AT TIME FOR CLOSING THE BORROWER CAN MAKE A TRANSFER FROM BUSINESS TO PERSONAL ACCOUNT.

400

Are these veterans ineligible for VA benefits? (True/False)

ACTIVE DUTY for 180+ days in training for reserves/national guard.

TRUE!!

They are not considered eligible!!

400

The USDA income limits are defined as the greater of % of the US median family income?

- 115% of the U.S. median family income for the area.

400

Interest rates are fixed and cannot be negotiated on DPA loans. True or False?

TRUE!!! You cannot decide the rate, the provider sends out the rates everyday.

500

Late Mortgage Payments for Purchase and No Cash-Out Refinance (TOTAL):

TRUE OR FALSE QUESTION.

The Mortgage must be downgraded to a Refer and manually underwritten if any mortgage trade line, including mortgage line-of-credit payments, during the most recent 12 months reflects:

NO 30 DAY LATE IN THE PREVIOUS 12 MONTHS.

FALSE!

• 3+ late payments of greater than 30 Days;

• 1+ late payments of 60 Days & 1+ 30-Day late payments; or

• 1+ payment greater than 90 Days late

500

Can a borrower purchase a home with NO CREDIT SCORE?

YES!!!! Lenders may submit loan casefiles to DU when no borrower has a credit score. DU will apply the following requirements:

The property must be a one-unit, principal residence, and all borrowers must occupy the property.

All property types are permitted, with the exception of manufactured housing.

The transaction must be a purchase or limited cash-out refinance.

The loan amount must meet the general loan limits—high-balance mortgage loans are not eligible.

The loan must be a fixed-rate mortgage.

The maximum LTV, CLTV, and HCLTV ratios are 90%.

The debt-to-income ratio must be less than 40%.

Reserves may be required as determined by DU.

A nontraditional credit history must be documented for each borrower without a credit score. See B3-5.4-03, Documentation and Assessment of a Nontraditional Credit History, for additional information.

500

What VA status disqualifies a borrower from getting VA benefits?

Dishonorable.

NOTE: The only acceptable character of service for a veteran who served in the Selected Reserves/National Guard is “HONORABLE”.

500

Interest Rates are typical slightly higher because the borrower has no skin in the game and since the mortgage insurance is lower?

TRUE OR FALSE?

FALSE!!

Interest rates for USDA loans are AMAZING! and sometimes even lower than your DPA loans.

500

What is % of the assistance a borrower can receive using CHENOA DPA?

3% - 5%