Definitions

Inventory

Reconciliation & Relizable

Depreciation

Misc.

100

Which of the following activities is not a component of the operating cycle?

a. Sale of merchandise

b. Payment of employees’ salaries

c. Collection of cash from merchandise sales

d. Purchase of merchandise

B. Payment of employees’ salaries

100

Reeves Company is taking a physical inventory on March 31, the last day of its fiscal year. Which of the following must be included in this inventory count?

a. Goods in transit to Reeves, FOB destination

b. Goods that Reeves has ordered and paid for, but have not yet been shipped by the supplier because they require additional manufacturing work before they are complete

c. Goods in transit that Reeves has sold to Smith Company, FOB shipping point

d. Goods that Reeves is holding in inventory on March 31 for which the related Accounts Payable is 15 days past due

d. Goods that Reeves is holding in inventory on March 31 for which the related Accounts Payable is 15 days past due

100

Which of the following bank reconciliation items would not result in an adjusting entry?

a. Service charge.

b. Deposits in transit.

c. NSF check of customer.

d. Collection of a note by the bank.

b. Deposits in transit.

100

Equipment that cost $144,000 and on which $120,000 of accumulated depreciation has been recorded was disposed of for $36,000 cash. The entry to record this event would include a

a. gain of $12,000.

b. loss of $12,000.

c. credit to the Equipment account for $36,000.

d. credit to Accumulated Depreciation for $120,000.

a. gain of $12,000.

100

In computing depreciation, salvage value is

a. the fair value of a plant asset on the date of acquisition.

b. subtracted from accumulated depreciation to determine the plant asset's depreciable cost.

c. an estimate of a plant asset's value at the end of its useful life.

d. ignored in all the depreciation methods.

c. an estimate of a plant asset's value at the end of its useful life.

200

Under a perpetual inventory system

a. accounting records continuously disclose the amount of inventory.

b. increases in inventory resulting from purchases are debited to purchases.

c. there is no need for a year-end physical count.

d. the account “purchase returns and allowances” is credited when goods are returned to vendors.

a. accounting records continuously disclose the amount of inventory.

200

A company purchased inventory as follows:

200 units at $6.00

300 units at $6.60

The weighted average unit cost for inventory is

a. $6.00.

b. $6.30.

c. $6.36

d. $6.40.

e. $6.60.

c. $6.36

200

In reviewing the accounts receivable, the net realizable value is $28,000 before the write-off of a $2,000 account. What is the net realizable value after the write-off?

a. $28,000

b. $2,000

c. $30,000

d. $26,000

a. $28,000

200

A plant asset was purchased some time ago on January 1 for $75,000 and had an estimated salvage value of $15,000 at the end of its useful life. The current year's depreciation expense is $5,000 calculated on the straight-line basis and the balance of the Accumulated Depreciation account at the end of the year is $25,000. The remaining useful life of the plant asset is

a. 15 years.

b. 12 years.

c. 7 years.

d. 5 years.

c. 7 years.

200

A company purchased land for $400,000 cash. Real estate brokers' commission was $25,000 and $45,000 was spent for demolishing an old building on the land before construction of a new building could start. The capitalized cost of land would be

a. $400,000.

b. $425,000.

c. $445,000.

d. $470,000.

d. $470,000.

300

The accounting principle that requires that the cost flow assumption be consistent with the physical movement of goods is

a. called the matching principle.

b. called the consistency principle.

c. nonexistent; that is, there is no such accounting requirement.

d. called the physical flow assumption.

c. nonexistent; that is, there is no such accounting requirement.

300

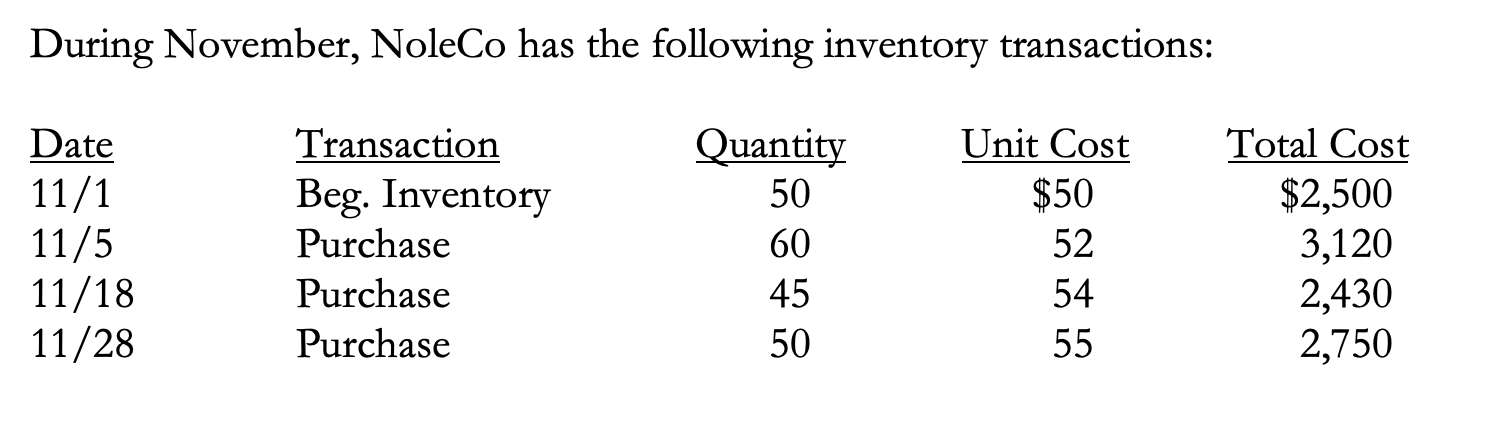

During November, NoleCo has the following inventory transactions:

During November, NoleCo sold 140 units at $75 each.

Under FIFO, Cost of Goods Sold equals

a. $3,560

b. $7,240

c. $3,280

d. $7,520

b. $7,240

300

Which of the following would be added to the balance per books on a bank reconciliation?

a. Outstanding checks.

b. Deposits in transit.

c. Notes collected by the bank.

d. NSF check.

c. Notes collected by the bank.

300

OBX Corp. purchased equipment for $750,000 on July 1, 20X1.

The estimated salvage value at the end of an estimated eight-year service life is expected to be $30,000. The equipment was operated for 1,500 hours in 20X1 and for 3,000 hours in 20X2. The company expects the machine to operate for a total of 15,000 hours over its eight-year life. OBX is a calendar year company that closes its books on December 31 each year.

Depreciation expense for 20X2 using the straight-line method equals

a. $96,430

b. $93,750

c. $90,000

d. $45,000

c. $90,000

300

A company collects a customer's accounts receivable balance within the discount period. Indicate how this transaction would affect (1) assets, (2) stockholders' equity, and (3) revenues.

A. (1) Decrease, (2) Decrease, (3) Decrease

B. (1) Increase, (2) Increase, (3) Increase

C. (1) Increase, (2) Increase, (3) No effect

D. (1) No effect, (2) No effect, (3) No effect

A. (1) Decrease, (2) Decrease, (3) Decrease

400

Which of the following is not an internal control activity for cash?

a. The number of persons who have access to cash should be limited.

b. The functions of record keeping and maintaining custody of cash should be combined.

c. Surprise audits of cash on hand should be made occasionally.

d. All cash receipts should be recorded promptly.

b. The functions of record keeping and maintaining custody of cash should be combined.

400

During November, NoleCo has the following inventory transactions:

During November, NoleCo sold 140 units at $75 each.

Under LIFO, Ending Inventory equals

a. $3,560

b. $7,240

c. $3,280

d. $7,520

c. $3,280

400

An analysis and aging of the accounts receivable of Watts Company at December 31 reveal these data:

What is the net realizable value of the accounts receivable at December 31 after year-end adjustment?

a. $2,740,000

b. $3,000,000

c. $3,200,000

d. $2,940,000

d. $2,940,000

400

OBX Corp. purchased equipment for $750,000 on July 1, 20X1.

The estimated salvage value at the end of an estimated eight-year service life is expected to be $30,000. The equipment was operated for 1,500 hours in 20X1 and for 3,000 hours in 20X2. The company expects the machine to operate for a total of 15,000 hours over its eight-year life. OBX is a calendar year company that closes its books on December 31 each year.

Depreciation expense for 20X2 using the double-declining balance method equals

a. $164,062.50

b. $157,500.00

c. $140,625.00

d. $93,750.00

e. $90,000.00

a. $164,062.50

400

Tony’s Market recorded the following events involving a recent purchase of inventory:

- Purchased goods for $100,000 on account, terms 2/10, n/30.

- Returned $2,000 of the shipment for credit.

- Paid $500 freight on the shipment.

- Paid the invoice within the discount period.

As a result of these events, the company’s inventory balance

a. increased by $98,000.

b. increased by $98,500.

c. increased by $96,540.

d. increased by $96,500.

c. increased by $96,540.

500

Which of the following is considered a cash equivalent for financial reporting purposes?

a. Accounts Receivable

b. Investments with maturity dates greater than three months

c. Checks received from customers

d. Accounts payable

c. Checks received from customers

500

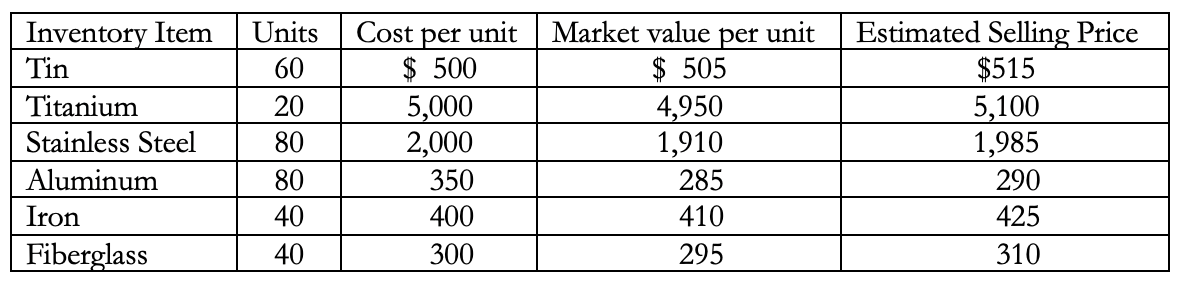

Whitman Corporation sells six different products. The following information is available on December 31:

When applying the lower of cost or net realizable value rule to each item, what will Whitman's total ending inventory balance be?

a. $346,000

b. $332,400

c. $333,100

d. $332,800

b. $332,400

500

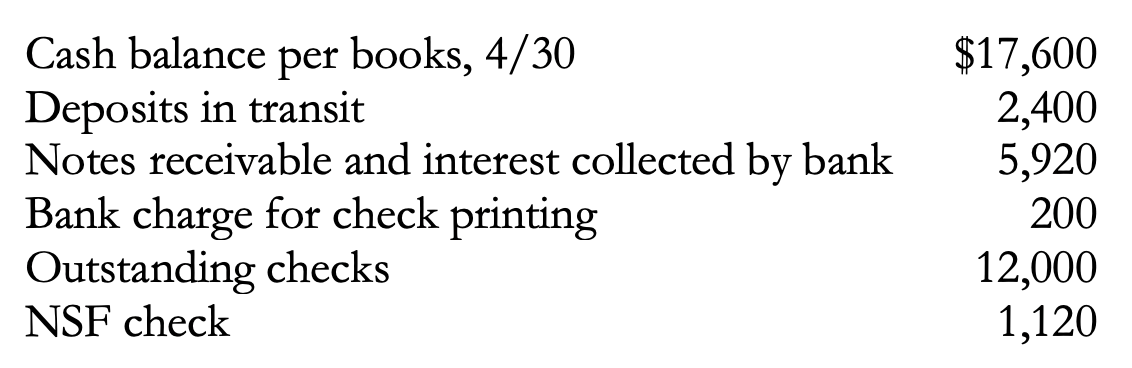

Karlin Company gathered the following reconciling information in preparing its April bank reconciliation:

The adjusted cash balance per books on April 30 is

a. $24,600.

b. $23,520.

c. $22,200.

d. $24,440.

c. $22,200.

500

OBX Corp. purchased equipment for $750,000 on July 1, 20X1.

The estimated salvage value at the end of an estimated eight-year service life is expected to be $30,000. The equipment was operated for 1,500 hours in 20X1 and for 3,000 hours in 20X2. The company expects the machine to operate for a total of 15,000 hours over its eight-year life. OBX is a calendar year company that closes its books on December 31 each year.

Depreciation expense for 20X2 using the activity-based method equals

a. $150,000

b. $144,000

c. $75,000

d. $72,000

b. $144,000

500

The following information is related to December 31, 20X1 balances.

During 20X2 sales on account were $870,000 and collections on account were $516,000. Also during 20X2 the company wrote off $48,000 in uncollectible accounts. An analysis of outstanding receivable accounts at year end indicated that $324,000 of receivables will be uncollectible. Bad debt expense for 20X2 is

a. $102,000.

b. $ 54,000.

c. $324,000.

d. $ 6,000.

a. $102,000.