Chapter 16

Chapter 17

More Chap 16

More Chap 17

Mystery

100

The statement of cash flows reports:

A. Cash flows from operating activities.

B. Significant noncash financing and investing activities.

C. All of the choices are reported on a statement of cash flows.

D. Cash flows from financing activities.

E. Cash flows from investing activities.

C. All of the choices are reported on a statement of cash flows.

100

The comparison of a company's financial condition and performance across time is known as:

A. Horizontal analysis.

B. Investment analysis.

C. Vertical analysis.

D. Political analysis.

E. Financial reporting.

A. Horizontal analysis.

100

The appropriate section in the statement of cash flows for reporting the purchase of equipment for cash is:

A. None of these. This is not reported on the statement of cash flows.

B. Investing activities.

C. Operating activities.

D. Financing activities.

E. Schedule of noncash investing or financing activity.

B. Investing activities.

100

One of several ratios that reflects solvency includes the:

A. Current ratio.

B. Total asset turnover.

C. Days' sales in inventory.

D. Times interest earned ratio.

E. Acid-test ratio.

D. Times interest earned ratio.

100

Chap 13 - Retained earnings:

A. Represent an amount of cash available to pay shareholders.

B. Can only be appropriated by setting aside a cash fund.

C. All of the choices are correct.

D. Generally consists of a company's cumulative net income less any net losses and dividends declared since its inception.

E. Are never adjusted for anything other than net income or dividends.

D. Generally consists of a company's cumulative net income less any net losses and dividends declared since its inception.

200

Cash flows from selling trading securities are usually reported in the statement of cash flows as part of:

A. Operating activities.

B. None of these. This is not reported in the statement of cash flows.

C. Noncash activities.

D. Financing activities.

E. Investing activities.

A. Operating activities.

200

The comparison of a company's financial condition and performance to a base amount is known as:

A. Risk analysis.

B. Horizontal ratios.

C. Financial reporting.

D. Vertical analysis.

E. Investment analysis.

D. Vertical analysis.

200

A statement of cash flows should reconcile the differences between the beginning and ending balances of:

A. Working capital.

B. Cash and cash equivalents.

C. Cash, cash equivalents, and short-term investments.

D. Equity.

E. Net income.

B. Cash and cash equivalents.

200

Quick assets divided by current liabilities is the:

A. Current liability turnover ratio.

B. Quick asset turnover ratio.

C. Working capital ratio.

D. Current ratio.

E. Acid-test ratio.

E. Acid-test ratio.

200

Chap 13 - The amount of income earned per share of a company's outstanding common stock is known as:

A. Dividends per share.

B. Book value per share.

C. Earnings per share.

D. Restricted retained earnings per share.

E. Continuing operations per share.

C. Earnings per share.

300

Which of the following transactions or events should be reported as a source of cash from operating activities when using the direct method?

A. Credit sales.

B. Cash received from the sale of treasury stock.

C. Cash collections from customers.

D. Depreciation expense.

E. Cash received from the sale of a building.

C. Cash collections from customers.

300

A financial statement analysis report:

A. Serves as a method of communication to users.

B. Helps users and preparers to refine conclusions based on evidence from key building blocks.

C. A financial statement analysis report entails all of the choices listed.

D. Forces preparers to organize their reasoning and to verify the logic of analysis.

E. Enables readers to see the process and rationale of analysis.

C. A financial statement analysis report entails all of the choices listed.

300

Which one of the following is representative of typical cash flows from operating activities?

A. Proceeds from collecting the principal amounts of loans.

B. Receipts of cash sales.

C. Proceeds from the issuance of bonds and notes payable.

D. Repayment of principals on loans.

E. Payments by a merchandiser to acquire equity securities of other companies.

B. Receipts of cash sales.

300

The common-size percent is computed by:

A. Dividing the analysis amount by the base amount.

B. Subtracting the base amount from the analysis amount and multiplying the result by 100.

C. Dividing the analysis amount by the base amount and multiplying the result by 100.

D. Dividing the base amount by the analysis amount.

E. Dividing the base amount by the analysis amount and multiplying the result by 1,000.

C. Dividing the analysis amount by the base amount and multiplying the result by 100.

300

Chap 14 - A bond sells at a discount when the:

A. Bond has a short-term life.

B. Bond pays interest only once a year.

C. Contract rate is above the market rate.

D. Contract rate is equal to the market rate.

E. Contract rate is below the market rate.

E. Contract rate is below the market rate.

400

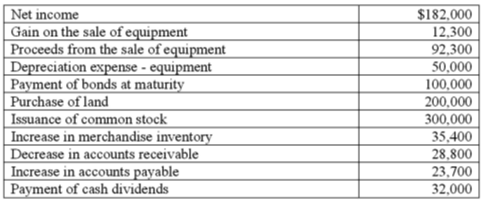

Weston is preparing the company's statement of cash flows for the fiscal year just ended. Using the following information, determine the amount of cash flows from financing activities:

A. $191,700.

B. $(168,000).

C. $(191,700).

D. $168,000.

E. $200,000.

D. $168,000.

400

A company's sales in Year 1 were $250,000 and in Year 2 were $287,500. Using Year 1 as the base year, the sales trend percent for Year 2 is:

A. 13%.

B. 115%.

C. 100%.

D. 87%.

E. 15%.

B. 115%.

400

When analyzing the changes on a spreadsheet used to prepare a statement of cash flows, the cash flows from operating activities generally affect:

A. Both noncurrent assets and noncurrent liabilities.

B. Noncurrent liability and equity accounts.

C. Equity accounts only.

D. Net income, current assets, and current liabilities.

E. Noncurrent assets.

D. Net income, current assets, and current liabilities.

400

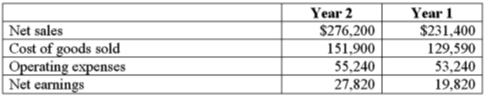

Use the following selected information from Farris, LLC to determine the Year 2 and Year 1 trend percents for net sales using Year 1 as the base.

A. 36.4% for Year 2 and 41.1% for Year 1.

B. 119.4% for Year 2 and 100.0% for Year 1.

C. 117.2% for Year 2 and 100.0% for Year 1.

D. 55.0% for Year 2 and 56.0% for Year 1.

E. 65.1% for Year 2 and 64.6% for Year 1.

B. 119.4% for Year 2 and 100.0% for Year 1.

Year 2: $276,200/$231,400 * 100 = 119.4%

Year 1: $231,400/$231,400 * 100 = 100.0%

400

Chap 12 - Collins and Farina are forming a partnership. Collins is investing a building that has a market value of $80,000. However, the building carries a $56,000 mortgage that will be assumed by the partnership. Farina is investing $20,000 cash. The balance of Collins' Capital account will be:

A. $44,000.

B. $24,000.

C. $80,000.

D. $56,000.

E. $60,000.

B. $24,000.

500

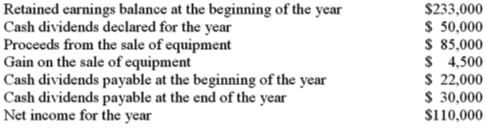

Woodlawn Company is preparing the company's statement of cash flows for the fiscal year just ended. The following information is available: The ending balance in retained earnings is:

The ending balance in retained earnings is:

A. $213,000.

B. $293,000.

C. $301,000.

D. $297,500.

E. $343,000.

B. $293,000.

500

Selected current year company information follows:

The return on total assets is:

A. 2.81%.

B. 6.28%.

C. 3.64%.

D. 4.67%.

E. 2.24%.

B. 6.28%

500

Sebring Company reports depreciation expense of $40,000 for Year 2. Also, equipment costing $140,000 was sold for its book value in Year 2. The following selected information is available for Sebring Company from its comparative balance sheet. Compute the cash received from the sale of the equipment.

A. $72,000.

B. $28,000.

C. $40,000.

D. $36,000.

E. $68,000.

B. $28,000.

Accumulated depreciation on equipment sold = $500,000 + $40,000 - $428,000 = $112,000

Cash received = $140,000 - $112,000 = $28,000

500

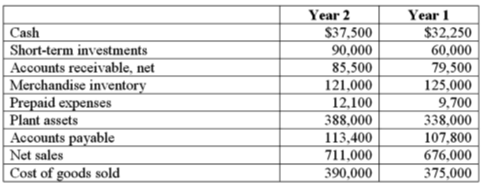

Refer to the following selected financial information from Fennie's, LLC. Compute the company's inventory turnover for Year 2.

A. 3.17.

B. 4.72.

C. 5.78.

D. 4.33.

E. 3.86.

A. 3.17

500

Chap 14 - A corporation borrowed $125,000 cash by signing a 5-year, 9% installment note requiring equal annual payments each December 31 of $32,136. What journal entry would the issuer record for the first payment?

A. Debit Interest Expense $11,250; debit Notes Payable $20,886; credit Cash $32,136.

B. Debit Notes Payable $32,136; debit Interest Payable $11,250; credit Cash $43,386.

C. Debit Notes Payable $11,250; credit Cash $11,250.

D. Debit Interest Expense $7,136; debit Notes Payable $25,000; credit Cash $32,136.

E. Debit Notes Payable $32,136; credit Cash $32,136.

A. Debit Interest Expense $11,250; debit Notes Payable $20,886; credit Cash $32,136.

Interest expense = $125,000 * 9% = $11,250; Principal reduction = $32,136 - $11,250 = $20,886