We Supply it

You Demand it

You Demand it

The idea that as price goes up, quantity demanded will decrease

The Law of Demand

What is given up as a result of making choices

Opportunity Cost

These are the two values that make up equilibrium

Quantity and Price

The fundamental problem of economics

Scarcity

Comparative advantage is not to be confused with this situation, where I can flat out produce more of something

Absolute Advantage

A movement ALONG the supply curve is a change in this.

Quantity Supplied

When one person can produce something with a lower opportunity cost

Comparative Advantage

One of these need to change in order to change the equilibrium

Supply or Demand

Name the four factors of production

Land, Labor, Capital, and Entrepreneurship

Identify one way in which trade benefits trade partners

*Access to more resources

*Makes possible to be outside of PPC

CONSUMER PREFERENCES and PRODUCTION COST are _____ of demand and supply respectively

Determinants

If Nolan can make 12 gallons of ice cream or 3 jars of peanut butter, this is his opportunity cost for making 1 gallon of ice cream.

1/4 a jar of peanut butter

If Supply shifts to the right, this is how price and quantity will change

Price decreases, quantity increases

Opportunity cost demonstrates this concept

Trade Off

If I have the comparative advantage in the production of a good, I will _______ and trade

Specialize

Name a determinant of demand

Market Size

Expectations

Related Prices

Income

Taste

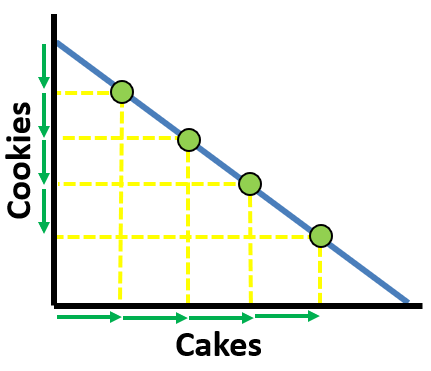

Draw a PPC on the board that demonstrates increasing opportunity costs

If supply increases, and Demand increase, this will definitely increase

Quantity

This means that the amount of one good you give up is always the same for every additional unit of another good you make

Constant Opportunity Cost

Without a change in available resources, mutually beneficial trade is the only way to achieve a point outside of this

PPC

Name a determinant of supply

Technology, Related Prices, Input Prices, Competition, Expectations

Draw a PPC on the board that represents constant opportunity costs

If a nations income decreases while simultaneously Technology is improving, then quantity will...

Be indeterminate

What inequality must be true in order for their to be a shortage

Qs < Qd or Qd > Qs or P < Pe

I can make 20 cars or 100 apples, you can make 30 cars or 90 apples. Identify MY opportunity cost for producing 1 apple

1/5 car