Formulas

Supply & Demand

Basics & Vocab

Graphs

FINAL JEOPARDY

100

In a factor market, Demand = ?

What is MRP?

100

This is the different quantities of workers that businesses are willing and able to hire at different wages.

What is the Demand for Labor?

100

The demand for resources is determined by the products they help produce

What is derived demand

100

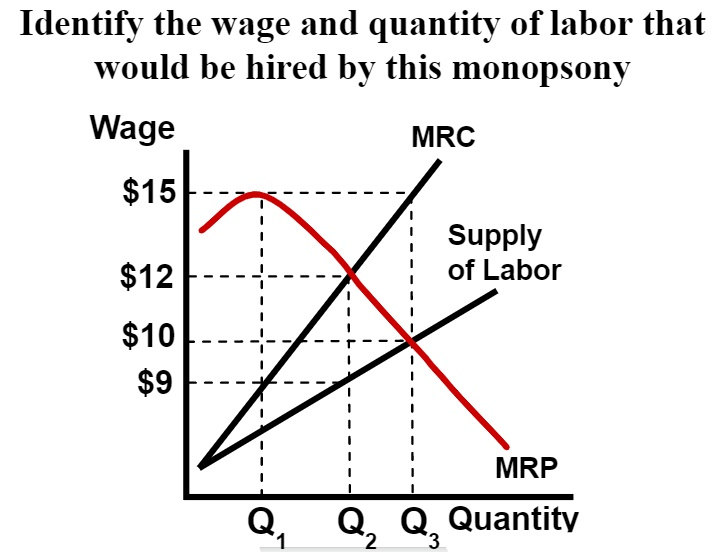

Wage=$9

Quantity= Q2

200

Profit maximization for a firm in a perfectly competitive labor market

MRC=MRP

200

There is a DIRECT (or positive) relationship between wage and

The quantity of labor supplied.

200

This law explains why each additional resource is less productive and therefore worth less than the previous one. Which is why the demand curve is downward sloping.

What is the Law of Diminishing Marginal Returns.

200

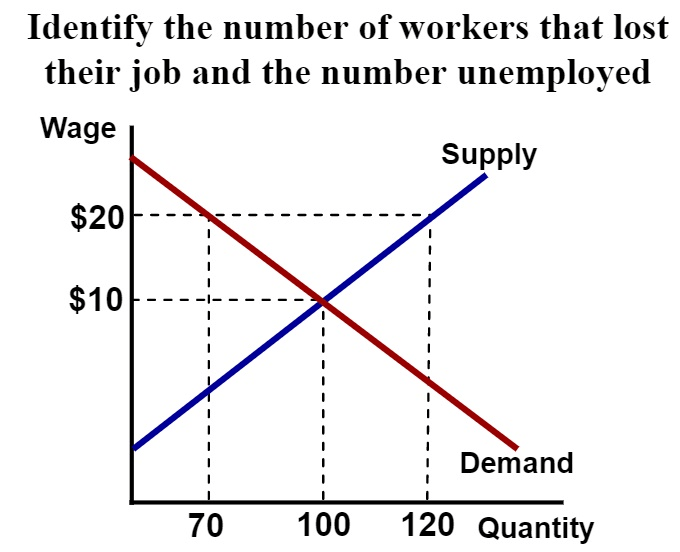

If the Government sets a minimum wage for $20, unemployment will increase by how many workers?

What is 50 workers?

300

The Change in Total Cost/ The Change in Inputs =

What is Marginal Resource Cost

300

These are the 3 SHIFTERS of DEMAND for LABOR

What are

1. Price of the output

2. Productivity of the worker

3. Change in the price of other resources

300

A lowest amount employers are allowed to pay their workers. It's a wage floor.

What is the minimum wage?

300

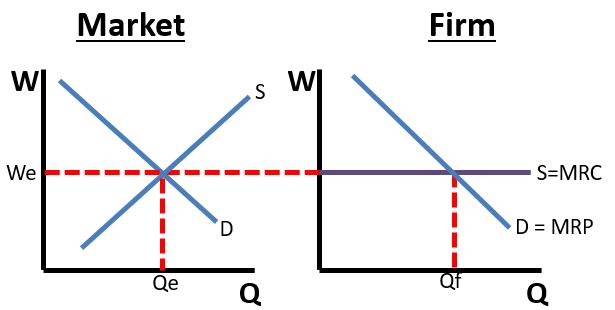

Graph a side-by-side graph of a PC labor market and firm

400

What is the least cost combination formula

MPl/Pl = MPc/Pc

or

MPx/Px = MPy/Py

400

List 4 of the 6 SHIFTERS of SUPPLY of LABOR

1. Education and training

2. Availability of alternative options

3. Immigration and mobility of workers

4. Cultural expectations

5. Working conditions

6. Preferences for leisure

400

These are the Four Factors of Production

Capital Entrepreneurship

Land Labor

400

What will happen to wages in a perfectly competitive labor market if there is a wage floor (minimum wage) imposed below equilibrium

nothing

500

This is the Profit Maximizing Rule for Combining Resources?

Marginal Revenue Product of Labor / Price of Labor = Marginal Revenue Product of Capital / Price of Capital = 1

or MRPx/Px = MRPy/Py =1

500

If there is an increase in the number of trained mechanics, what will happen to the wage and quantity of mechanics?

Wage - Decrease

Quantity - Increase

500

a market situation in which there is only one buyer of a resource/factor or only one employer

What is a Monopsony?

500

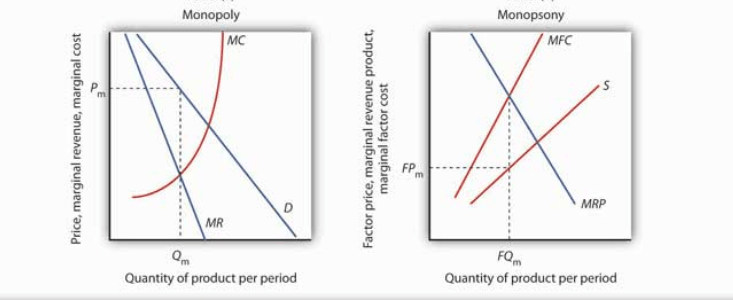

Graph a side-by-side graph of a monopoly and a monopsony

500

Assume the production of cell phones requires labor and capital. Currently the MRP for the last unit of labor is $20 and the MRP of the last unit of capital is $300. If the price of labor is $50 and the price of capital is $200, what needs to happen to the quantity of labor and the quantity of capital to maximize profit? Show your work and explain your answer.

The firm wants the MRP to equal the MRC for both labor and capital. For labor, the MRP is less than the MRC so the firm should decrease the amount of labor until MRP=MRC. For capital, the MRP is greater than the MRC so they should increase the amount of capital. To maximize profit with a combination of resources, the ratio of MRP/MRC for all resources should equal 1.