Vocabulary

Multiple Choice

Vocabulary 2

Formulas

Misc

100

Type of firm that involves combining Direct Materials, Direct Labor, and Overhead to make a product.

Manufacturing

100

Actual or Normal Costing:

applies overhead through a predefined overhead rate.

Normal Costing

100

Accumulated Costs are assigned to units of products manufactured or services delivered

Cost Assignment

100

(V.MOH + F. MOH) / Activity Level

Predetermined Overhead Rate

100

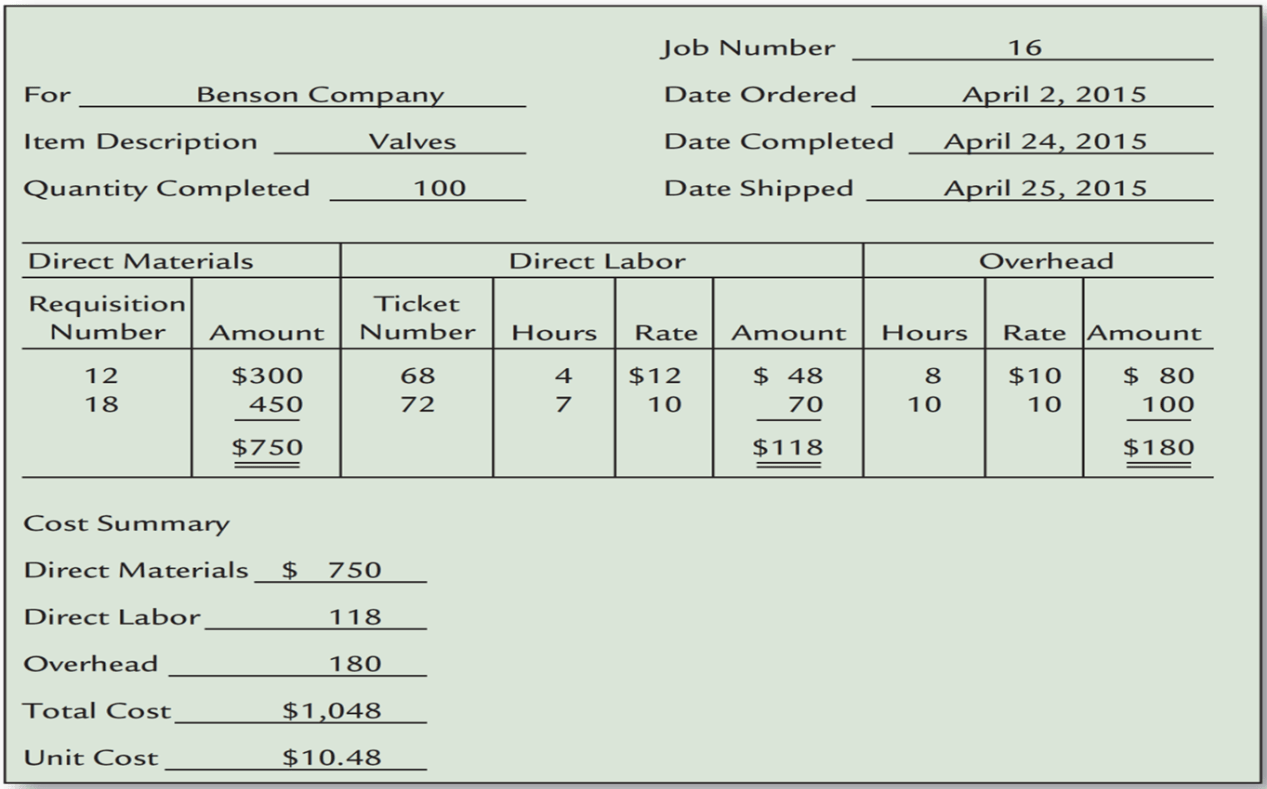

The image below is an example of?

Job Order Cost sheet

200

The accounting system satisfies the need for cost accumulation, cost measurement, and cost assignment.

Cost Accounting System

200

Normal or Expected Activity Level:

The average activity usage that a firm experiences in the long term.

Normal Activity Level

200

The production level that a firm expects to attain for the coming period

Expected Activity Level

200

Total Manufacturing Cost / # of Units Produced

Unit Cost

200

This cost is debited to the overhead control account

Actual Overhead expenses

300

Uses actual costs for direct materials direct labor and overhead to determine unit cost

Actual Costing

300

Debit or Credit:

To close the overhead variance account for under-applied overhead, do you debit or credit the account

Credit

300

Absolute maximum production activity of a manufacturing firm

Theoretical activity level - .

300

TMC / # of Units

Total Manufacturing Cost

300

The method utilized to assign costs to products or services

Cost Measurement

400

Uses actual costing , plus applies overhead using a predetermined rate to determine unit costs

Normal Costing

400

Normal Spoilage or Abnormal Spoilage:

Arises from the nature of the production process

Normal Spoilage

400

Follows costs from the point at which they are incurred to the point at which they are recognized as an expense on the income statement.

Cost Flow

400

Compute the predetermined overhead rate for a firm that has estimated overhead costs for the coming year at $900,000 and expected activity is 90,000 DLH

10 per DLH

900,000 / 90,000

400

Immaterial under or applied overhead is closed to this account

COGS