Think Theory

Formats & Formula

Account in Action

100

Why is depreciation provided?

To spread the cost of an asset over its useful life

100

Which section will depreciation be under in the income statement?

Expenses

100

At 31 December 2020, the cost of motor vehicles is $30,000 and its accumulated depreciation is $9,000. Reducing balance method for 20% is used to calculate its depreciation. What is the depreciation of motor vehicles for the year ended on 31 December 2020?

$4,200

200

State four causes of depreciation of non-current assets

-Physical deterioration/wear and tear

-Economic reasons

-Passage of time

-Depletion

200

How do you find depreciation using the reducing balance method?

(Cost - Accumulated Depreciation) x Depreciation Percentage//Net Book Value x Depreciation Percentage

200

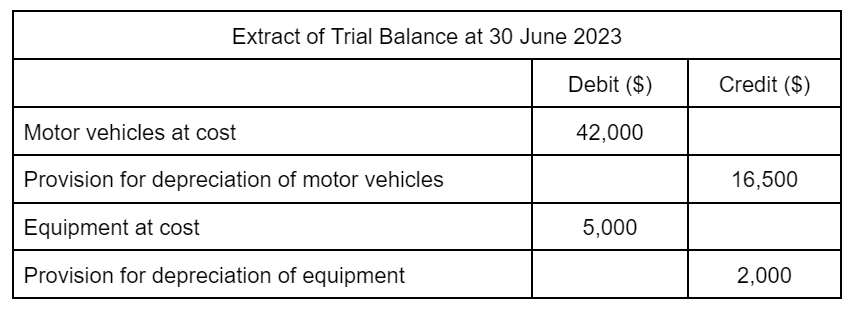

Depreciation is to be charged on motor vehicles at 25% per annum using the reducing balance method. Meanwhile, depreciation on equipment is to be charged at 20% per annum using the straight-line method. What is the total depreciation for the year?

$7,375

300

Explain the reducing balance method of depreciation

The same percentage is written off each year but it is calculated on the net book value of the asset//The depreciation charged that decreases each year as it is calculated on the net book value rather than the cost

300

On 1 July 2013 Alice purchased fixtures costing $25,000 and paid by cheque. She estimated that she would be able to use the fixtures for four years and then be able to sell them for $3,000. What is the formula to find the depreciation charge?

(Cost of Asset - Residual Value) ÷ Number of years of expected use//($25,000-$3,000) ÷ 4 years = $5,500

300

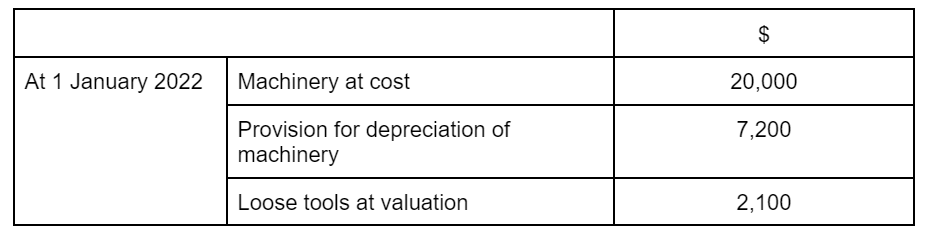

Machinery is depreciated at 20% per annum using reducing balance method, Additionally, loose tools were purchased during the financial year. On 31 December 2022, loose tools more than 12 months old were valued at $1850. What was the depreciation charge for the year ended 31 December 2022?

$2,560 (Machinery) and $250 (Loose tools)//$2,810

400

Explain how charging depreciation is an example of the application of the principle of prudence and matching

PRUDENCE: Ensures that non-current assets are shown at more realistic values//Ensures that the profit for the year is not overstated

MATCHING: The cost of the non-current asset and the revenues arising from its use are matched in an accounting period//The cost of the non-current asset is spread over its useful life

400

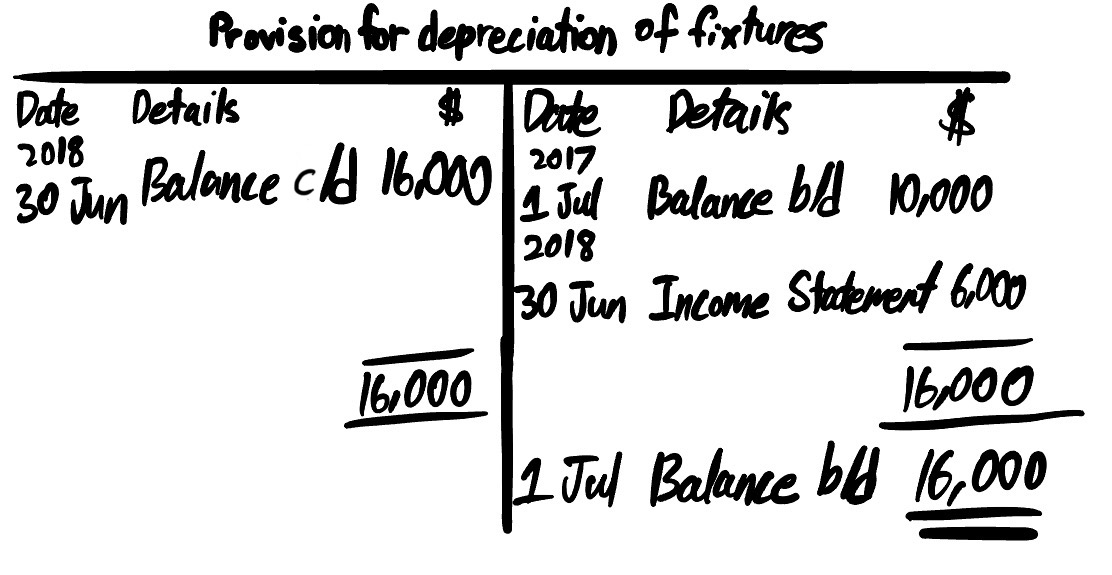

Arrange the following information into the depreciation account:

400

M Limited’s financial year ends on 31 December. He depreciates his equipment at 20% per annum using straight-line method.

M Limited provided the following information:

1 January 2015 Purchased equipment A for $15,000 and equipment B for $18,000

1 July 2017 Equipment A was sold for $8,600. On the same date, equipment C was purchased for $21,000

What is the depreciation charged for the year?

$7,800

500

Suggest one reason why the loose tools are revalued at the end of each financial year rather than by using the straight line or reducing balance method of depreciation

The individual tools may not cost enough to treat them as separate non-current asset//Not practical or difficult to keep detailed records of such assets

500

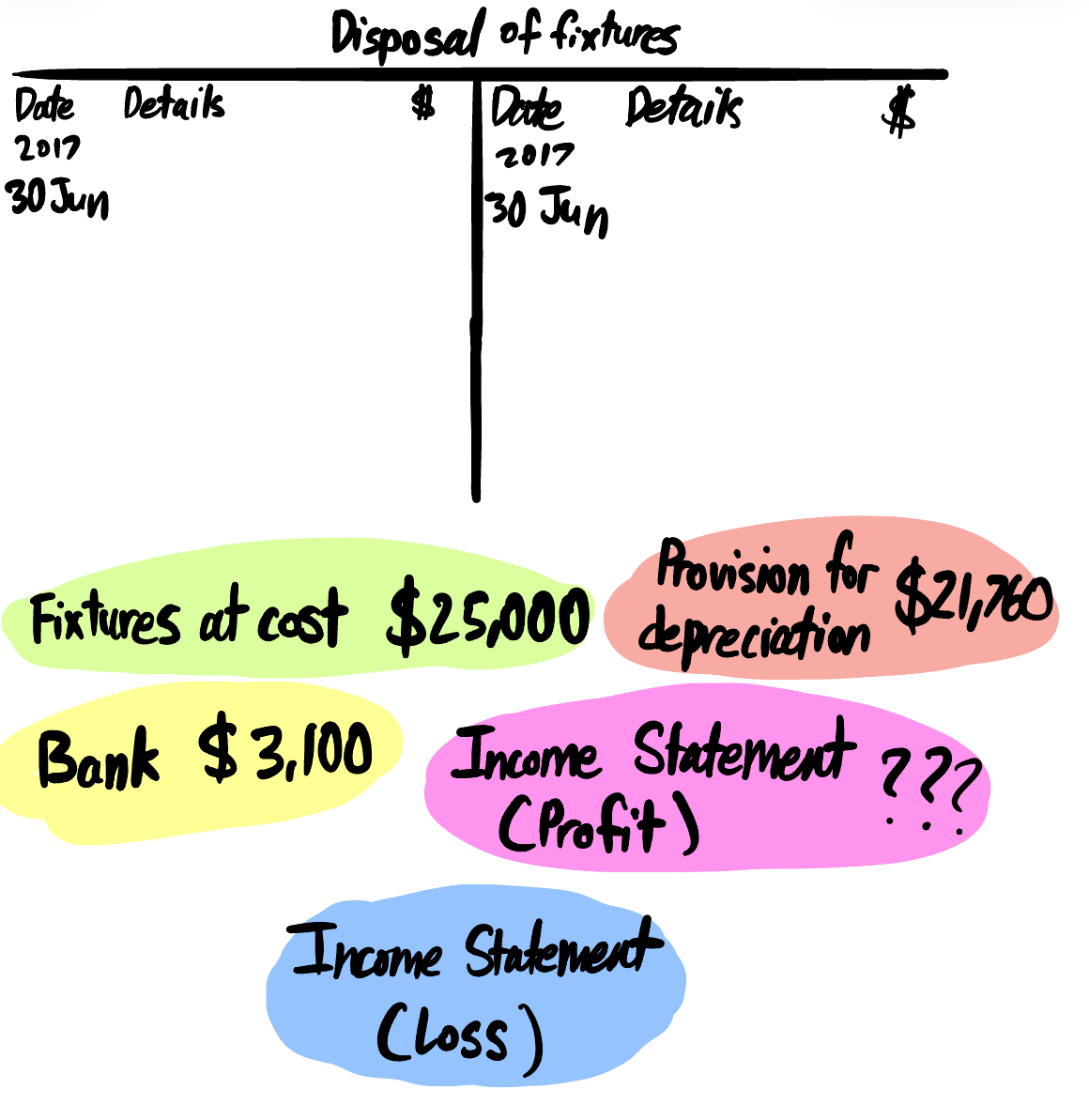

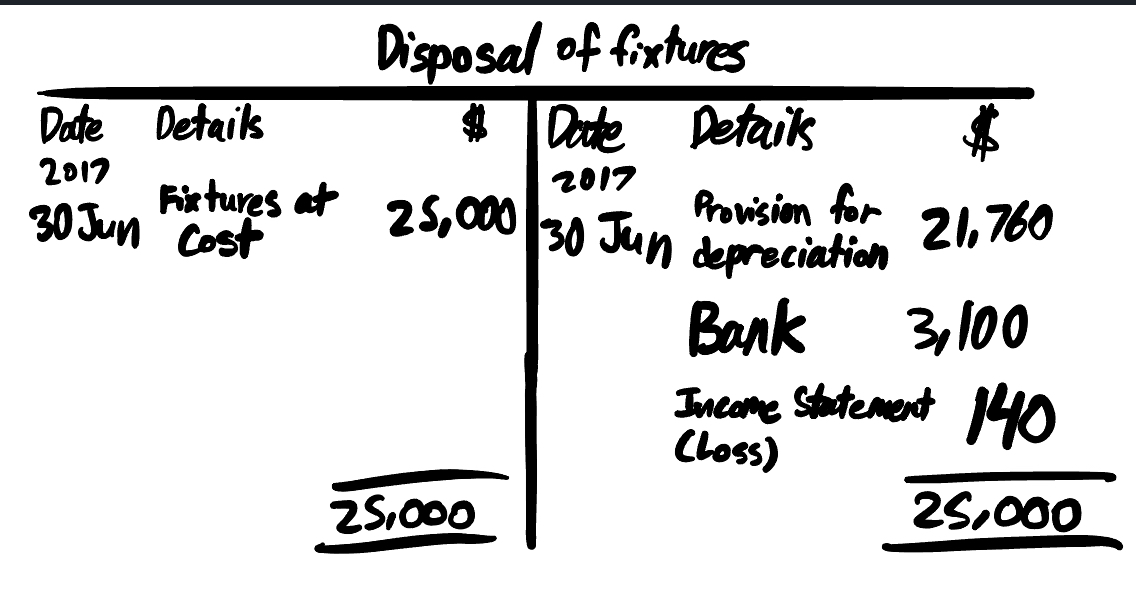

Arrange the following information into the disposal account:

500

Chibuzo’s financial year ends on 31 December. He depreciates his motor vehicles at 20% per annum on the cost of motor vehicles held at the end of each financial year.

Chibuzo provided the following information:

1 January 2017 Purchased motor vehicle A for $15,000 and motor vehicle B for $18,000

1 July 2019 Motor vehicle A was sold for $8,600. On the same date, motor vehicle C was purchased for $21,000

Calculate the profit or loss on disposal of motor vehicle A.

$400 (loss)