introduction to Economics

Demand, Supply, Market Equilibrium

P.E.D, P.E.S, Y.E.D

Externalities, Public Goods

GDP,GNI

100

Fill in the blank space

Social sciences study societies and the ........................................ within those societies

Human Interactions

100

Differentiate between Demand and Supply

Demand is the willingness backed by the ability of consumers to buy goods and services at a given price in a given period,

while supply is the willingness and ability of producers to sell/produce goods and services at a given price in a given period of time.

100

Define Income Elasticity of Demand

This measures the responsiveness of a change in quantity demanded as a result of a change in income.

100

Mention 2 reasons why governments intervene

1. To correct market failure

2. Collect Government Revenue

3. Support poorer households

4. Support Firms

100

National income accounting measures the .............................................. within a country and provides insights into how a country is performing

Economic Activity

200

Mention 1 difference between MicroEconomics and MacroEconomics

Microeconomics is the study of individual markets and sections of the economy, rather than the economy as a whole, while Macroeconomics is the study of economic behaviour and decision making in the entire economy, rather than just an individual market

200

Describe the law of demand

The Higher the Price the lower the quantity demand, and the lower the price the higher the quantity demanded.

200

List two factors that influence the elasticity of demand for a product.

1. Availability of substitutes

2. Addictiveness of the product

3. Price of product as a proportion of income

200

The following diagram describes one of the two types of taxes studied. Which one is it?

Specific Tax - A specific tax is a fixed tax per unit of output (specific amount)

200

Mention 2 leakages in the circular flow of income

1. Savings

2. Taxes

300

Once upon a time, in a small village nestled between rolling hills, there was a thriving farm called Green Valley, known for its lush wheat fields, juicy apples, and happy cows that produced the creamiest milk. Run by the hardworking Green family and their loyal farmhand, Sam, the farm decided to expand by acquiring 10 acres of fertile land, hiring five more helpers, and investing in new equipment like a tractor and irrigation system, along with seeds, fertilizer, and cow feed. With these additions, the farm flourished even more, doubling its wheat harvest, growing its apple orchard, and producing enough milk to supply the entire village and beyond.

Identify three factors of production in this story:

Land: The additional 10 acres of fertile land with rich soil used for growing wheat and vegetables.

Labor: The five new helpers from the village, along with Sam and the Green family, who provided the physical effort to plant, harvest, and tend to the cows.

Capital: The new equipment (tractor and irrigation system), seeds, fertilizer, and cow feed purchased to improve and expand the farm's operations.

300

Mention two non-price determinants of demand

1. Change in Income

2. Change in the price of Substitutes

3. change in taste and preference

4. Change in the number of consumers/change in population

300

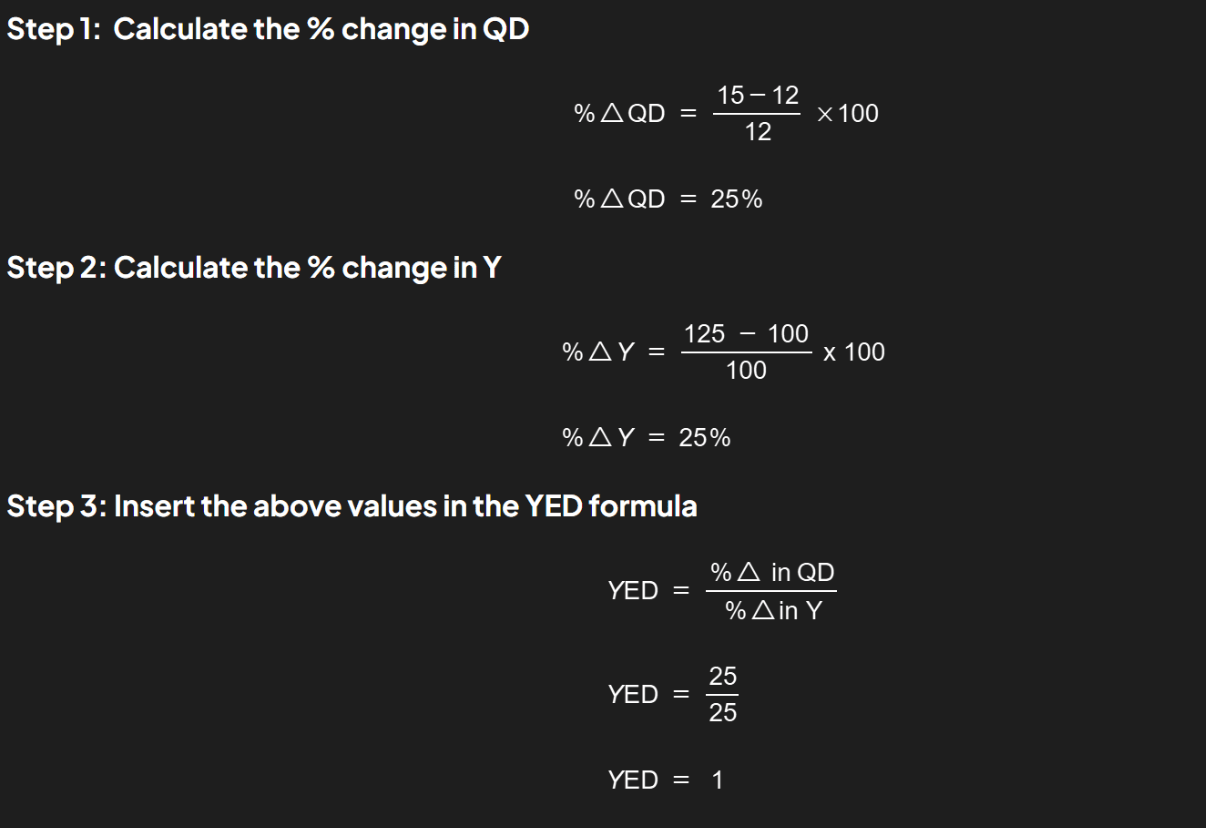

A consumer's income rises from RMB 100 to RMB 125 a week. They originally consumed 12 bubble teas but this increased to 15 bubble teas a week. Calculate the YED of the bubble teas

300

Congratulations! You won free 300 bonus points for your group.

300

Three Approaches to the Calculation of National Income

1. Output Approach

2. Income Approach

3. Expenditure Approach

400

Joyce wants to visit her best friend in Ghana

She looks at flight prices from London to Accra

On Friday night it costs £500 whereas Thursday night is only £350

She is about to book the Thursday flight but then realises that the opportunity cost of saving £150 on a flight is the inability to work on Friday (loss of £380 income)

She books a cheaper flight. What is the opportunity cost of her decision

Loss of income of £380

400

When there is an increase in the cost of fertilizer for the production of apples, how will that affect the equilibrium price and quantity demand for the market for apples?

An increase in the cost of fertilizer raises production costs for apples, reducing supply. This shifts the supply curve leftward, leading to a higher equilibrium price and a lower equilibrium quantity demanded for apples.

400

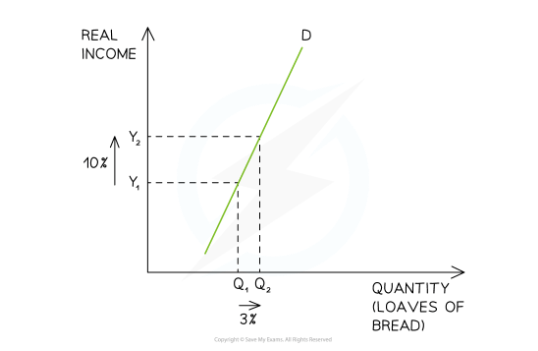

What type of goods does this diagram suggest?

Normal Good - Necessity

400

Mention two Advantages of Indirect Taxes

1. Raises revenue for government programs

2. Raises the price and reduces the quantity demanded of demerit goods.

400

Differentiate between GDP and GNI

GDP (Gross Domestic Product): Measures the total value of all goods and services produced within a country's borders over a specific period, regardless of who owns the production factors (e.g., labor, capital).

GNI (Gross National Income): Measures the total income earned by a country's residents and businesses, including income from abroad, but excluding income earned by foreign entities within the country.

500

Identify the attainable points on the PPC

Attainable Points are points B, C, D, A

500

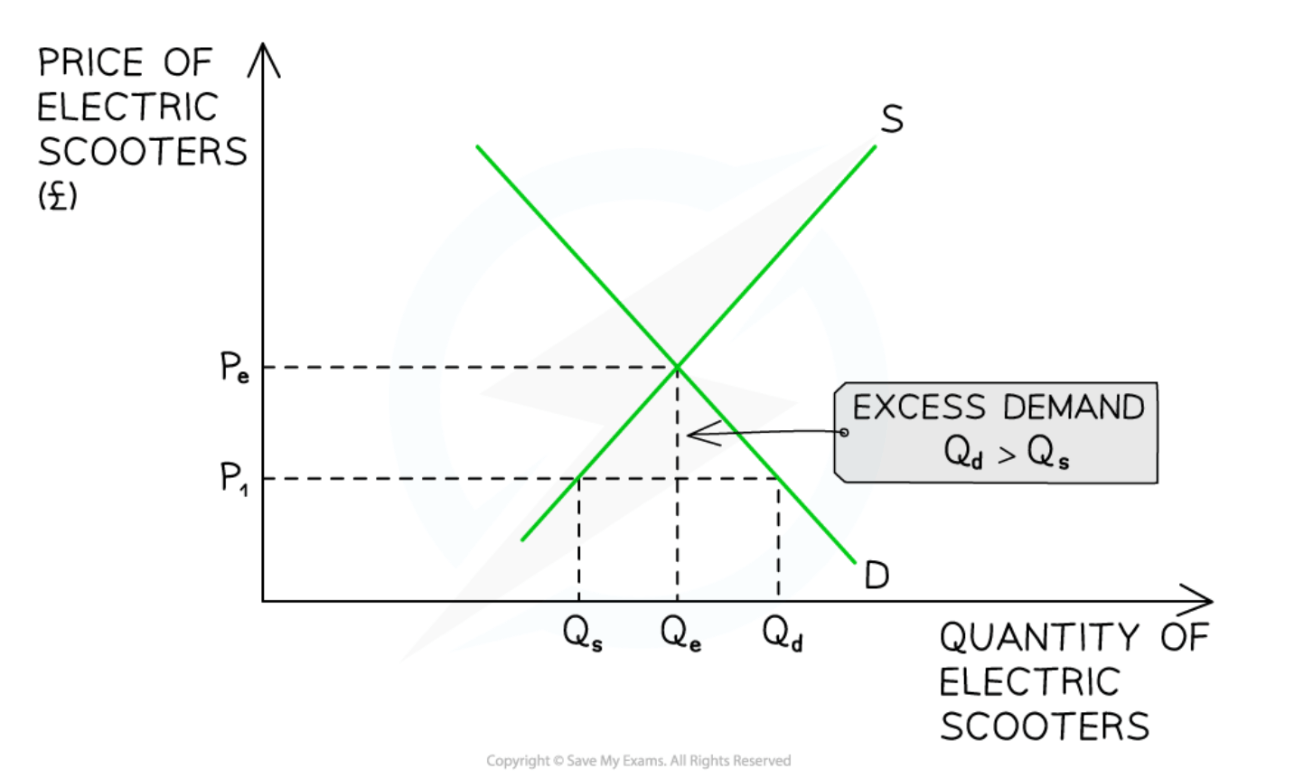

The picture above shows excess demand. Explain how the market responds to correct itself.

Excess demand shows there is a disequilibrium. The price is set below the equilibrium point and there is greater demand than supply.

Sellers realise they can increase prices and generate more revenue and profits

Sellers gradually raise prices

In time, the market will have cleared the excess demand and arrive at a position of equilibrium, PeQe

500

Describe one importance of P.E.D. to the business/firm

P.E.D. is important to the business/firm because when the P.E.D. is elastic it suggests that a slight increase in price will lead to a proportionately larger decrease in quantity demanded. This means that revenue of the firm will decrease. This will also reduce their profits.

500

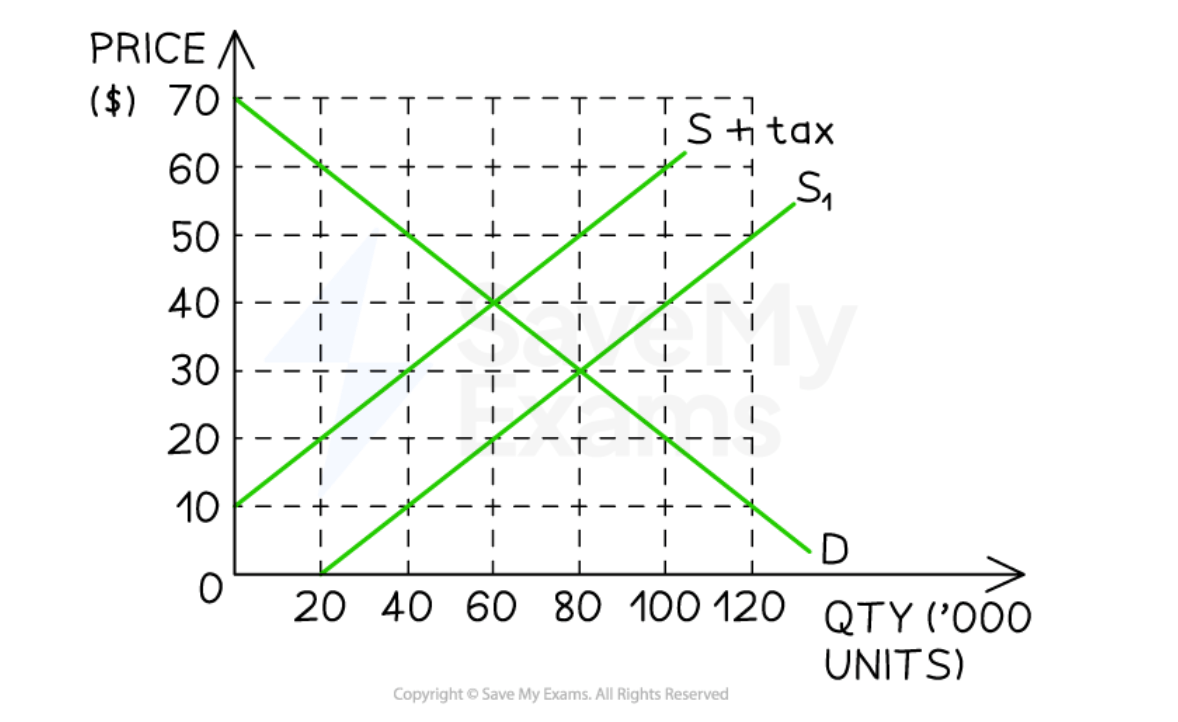

The Government imposes a tax of £20 on a product. Calculate the tax revenue collected by the government.

500

You won this. Well done!!