Core PR Concepts

Compliance/Research/Resources

Calculation of paycheck

PR Process/Supporting systems/Admin

PR Admin/Management

Audits

Accounting

100

the 2 common worker classifications

employees and independent contractors

100

definition of escheatment

turning unclaimed property over to state

100

definition of Regular Rate of Pay:

An hourly pay rate determined by dividing the total regular pay actually earned for the workweek

by the total number of hours worked.

100

ROP definition

Request for Proposal

100

in situational leadership - way managers handled their staffs often depended on the way they dealt with two factors

task behavior and relationship behavior

100

what are common payroll audits

401K

section 125

wage & hour

unemployment

100

several business areas that use data provided by

the payroll department

General accounting uses payroll data to record transactions in the company’s books of account and to prepare

financial statements both for internal and external purposes.

• Cost accounting uses payroll data to determine the cost of producing a product or providing a service and to

show ways of controlling these costs (e.g., wage data used to determine the cost of labor).

• Budgeting involves projecting the costs and revenues associated with various business activities and trying

to keep the costs—including

payroll costs—within

target limits.

200

the FLSA establishes

Minimum wage

Overtime pay

recordkeeping

child labor standards

200

requirements you may

be subject to include when working in payroll

• Family and Medical Leave Act (FMLA) eligibility and tracking

• Fair Labor Standards Act (FLSA) compliance for overtime, including average rate calculations

• Affordable Care Act (ACA) eligibility and reporting

• Sarbanes-Oxley

Act

• State overtime, meal and break, and FMLA rules

• Multiple workstate and local tax jurisdiction compliance

• For global installations, the regulations in other regions or countries

200

definition of a work week per FLSA

A workweek consists of seven consecutive 24-hour periods that equal 168 total hours

200

time & attendance automation benefits

Less time spent on processing

Fewer errors introduced during processing

Decreased costs

200

different management

styles per Hersey and Blanchard

• Low task/high relationship—little

control sought by the manager; good deal of mutual trust and support.

• High task/high relationship—manager

controls the job and procedures; also relies on personal communication

with employees to coach them in performing the job.

• Low task/low relationship—most

jobs delegated to staff; little personal contact desired by manager.

• High task/low relationship—manager

seeks to control staff and direct performance; but with little feedback

or dialogue with employees.

200

Check Payment Controls

Update signature authorizations

Hand checks to employees

Lock up undistributed paychecks

Match addresses

Payroll checking account

200

accounting time period concept

Each organization must determine its own accounting period based on the type of business it is

engaged in. For its yearly accounting period, an organization can choose either the calendar year or another 12-month

period (fiscal year, e.g., 6-1-

17

to 5-31-

18).

In most organizations, the end of the fiscal year coincides with the least

business activity for the year.

Printed for:

300

the federal minimum wage and when was it established

$7.25 per hour and 7.24.09

300

Internal Revenue Code requires all employers to withhold what taxes from employees pay

federal income, social security, and

Medicare taxes

300

IRS regulations include several fringe benefits examples

• Employer-provided

cars

• Flights on employer-provided

aircraft

• Free or discounted commercial flights

• Vacations

• Discounts on property or services

• Employer-paid

memberships in country clubs or other social clubs

• Tickets to entertainment or sporting events

• Qualified tuition reductions

• Dependent care assistance

• No-additional-

cost

services

• Working condition fringes

• Qualified transportation fringes

• De minimis fringes3

300

reports payroll manager may be required to produce

• New legislative and/or regulatory developments, such as new tax rates or wage bases, new rules governing

employee business expenses, or changes in the way states treat employee benefits

• Monthly labor costs—pay

rates, regular and overtime hours worked, compensation, paid time off, etc.

• Annual wages, taxes, and benefits

• Variance between compensation paid and budgeted

• Reports required from all department heads detailing ongoing projects, overtime pay, salary costs, future

plans, budgets, etc.

• Metrics measuring payroll processing costs overall and at different points in the process (e.g., gathering

time and attendance information)

300

payroll, we can assess our strength by asking a series of questions

• How well do we do our jobs?

• Do we provide accurate information?

• Is our final product accurate?

• Do we serve our customers well?

300

payroll calculation controls

Automated timekeeping systems

Calculation verification

Hours worked verification

Match payroll register to supporting documents

Match time cards to employee list

Overtime worked verification

Pay change approval

300

accounting equations

Assets -Liabilities= Equity

Revenue -Expenses= Net Income

Net Income -Income Distributed + Contributed Capital = Equity

400

the definition of exempt per FLSA

exempt from the OT provisions of the FLSA

400

meaning of acronyms: IRC and IRS

Internal revenue code

internal revenue service

400

involuntary deductions are and 2 examples

those over which an employer or employee has no control

tax levies

student loans

400

qualities that can help make a payroll manager a strong leader include

• Having a vision. A strong payroll manager must have a clear vision of where the manager and the department

should be headed, what their mission is, and how that vision and mission blend in with those of

the overall organization. With a vision of quality service, everyday work, which can seem mundane and

ordinary at times, becomes more purposeful and exciting. A leader must also communicate that vision, be

prepared for those who challenge it, and then acquire the resources to achieve the vision.

• Building team support. Without the support of the department’s employees, the manager’s goals and vision

will be unreachable. The payroll manager can build team support by creating an atmosphere where employees

are treated fairly, their ideas are given thoughtful consideration, and their needs are deemed important

and worth meeting.

• Seeking partners. Payroll managers cannot exist apart from the rest of the company. To be leaders, they must

network and seek the advice and support of managers from other departments.

• Accepting accountability. Leaders accept accountability for things that happen by owning the outcome. They

admit when a mistake was made or a problem is found in the payroll process and take ownership of it until

the problem is solved. Leaders also make good on their commitments and acknowledge the contributions

of other staff members rather than taking undue credit for themselves.

• Making decisions and taking action. Good leaders are decisive and then take action to put their decisions

into practice. Deciding what’s wrong with a practice or procedure in payroll will not solve anything unless

action is taken to put a solution in place.

• Leading by example. To be a leader, the payroll manager must take the initiative and be the first one to step

forward when a difficult problem needs solving or a crisis looms. Leading by example also means acting

with integrity by following your principles even when the consequences may not be pleasant.

400

planning and organizing consists of several key activities

Defining goals and objectives

Defining the time frame

Defining the subtasks

Analyzing available resources

Evaluating costs

400

general payroll controls

audit

change authorizations

change tracking log

error-checking reports

expense trend lines

issue payment report to supervisor

restrict access to records

separation of duties

400

typical company expenses include

• Wages paid to employees

• Employer-paid

benefit costs

• Maintenance for computers

• Office supply costs

• Employer share of payroll taxes

500

joint employer status under the FLSA

an employee’s hours worked for both employers for the workweek must be aggregated and considered as one

employment when determining whether any overtime pay is due

500

the 3 deposit schedules for federal withheld payroll taxes

monthly and semi-weekly and next day

500

federal taxes employer pays and 2019 limits including percentage

7.65% FICA 6.2% Social Security $132900 and 1.45% Medicare

FUTA 6.0% $7000 state credit 5.4%

500

critical resources needed to continue the payroll function in event of disaster include

• Staff

—— Travel/Lodging arrangements

—— Work location –disaster

recovery facility

—— Support from key business units including IT staff

• Equipment

—— Electronic and network connectivity

—— Systems or applications

—— Instructions or manuals (physical or electronic records) or other vital records

—— Ability to print checks, process direct deposits, and/or issue/update paycards

• Others

500

five steps to empowerment

• Step 1: Establish the desired results. The expected results are that the employees will have their pay corrected

with a manual check, their future paychecks will be adjusted properly, and they will receive quality customer

service.

• Step 2: Provide guidelines. The manual checks must comply with all applicable federal, state, and local

requirements, as well as company policies.

• Step 3: Identify resources available to accomplish the task. The following information is provided: tax tables,

company policies on manual checks, wage and hour guidelines, and contacts who can handle questions.

• Step 4: Hold people accountable. The employee will be evaluated based on the satisfaction level of employees

receiving the manual checks and the degree of compliance with the guidelines that have been provided.

• Step 5: Identify consequences. If the employee fails to complete the task timely and accurately, the company

will be exposed to possible financial penalties, the reputation of the payroll department in the organization

will suffer, and the failure will be noted on the employee’s performance record.

500

actions that can be taken for improving the payroll process performance:

• System review, evaluation, and updating

• System edits

• Account balancing and reconciliation

• Documentation of policies and procedures

• Internal controls, such as job segregation, job rotation, file security, physical payouts, etc. (see Section 11.8)

• External audits

500

Some transactions that represent liabilities include

• Income and employment taxes withheld but not yet deposited

• Contributions owed to a company benefit plan

• Accounts payable

• Wages payable

• Union dues deducted from pay but not yet paid to the union

600

SS8

Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding

600

The Walsh-Healey

Public Contracts Act376

governs the wages and hours of employees of manufacturers and dealers

furnishing the federal government with materials, supplies, and equipment under contracts exceeding $10,000.

600

gross up formula without 401K and example including calculation and proof

100 minus fit minus ss minus medi equal result

gross divided by result percentage

proof

600

Selecting a paycard vendor considerations

Type of card—Decide

whether the employer will use branded or nonbranded cards.

Employer costs—There

are several types of employer costs associated with paycards, including setup fees (e.g., creating

accounts, enrolling employees), payroll processing costs, and extra fees for one-time

payments (e.g., off-cycle

payments,

termination payments).

Employee costs—There

may be different costs for ATM and POS transactions depending on the vendor. Some of them

may waive the fee for the first transaction each pay period, and there may be added fees for extra services, such as

monthly statements or balance checks.

Legal issues—Make

sure that any vendor you are considering can comply with the wage payment regulations in the

states where the organization operates.

System compatibility—Make

sure that the vendor’s system is compatible with your employer’s payroll system.

Training—Determine

if the vendor offers training both for the payroll department on the software involved and for the

employees who will be using the paycards.

Paycard implementation issues.

600

easiest ways for a company to lose control over its entire payroll system

is to rely on verbal communication

of policies and procedures.

600

Controlling the process to improve performance actions

• System review, evaluation, and updating

• System edits

• Account balancing and reconciliation

• Documentation of policies and procedures

• Internal controls, such as job segregation, job rotation, file security, physical payouts, etc. (see Section 11.8)

• External audits

600

definition of debits and credits in accounting

A debit is an accounting entry that either increases an asset or expense account, or decreases a liability or equity account. It is positioned to the left in anaccounting entry. A credit is an accounting entry that either increases a liability or equity account, or decreases an asset or expense account

700

SS5

Application for Social Security card

700

Davis-Bacon

and Related Acts

the Secretary of Labor sets prevailing minimum wage standards for laborers

and mechanics working on federally financed construction contracts of $2,000 or more. The “Related Acts” include

provisions that require Davis-Bacon

labor standards be applied to most federally aided construction. The prevailing

wages (including fringe benefits) are based on wages for similar workers in the locality where the project is to take place.

700

Shortened Formula gross up formula (when social security wage base has already been exceeded):

X = [Desired Net –.

009 ($200,000 –YTD

Medicare wages)]/.7565

X = [$30,000 –.

009 ($200,000 -$

175,000)]/.7565

X = [$30,000 –.

009 ($25,000) /.7565

X = [$30,000 –$

225]/.7565

X = $29,775/.7565

X = $39,358.89

700

What is a Business continuity plan

Because of the dangers of having a computer

system with the associated data all in one place should a disaster hit (e.g., fire, blackout, electrical storm),

sound business practice requires the employer to have a payroll business continuity plan that has been

tested and is ready to use (see Section 12.6). (It should be a part of any automated payroll system.)

• Wrong computer chosen. Despite all the investigation and research done before purchasing payroll system

software and/or hardware, it may prove to be inadequate or have too much capacity for the employer’s needs

700

Payroll managers in mid-size

and large organizations responsibilities

planning, staffing, training, evaluating,

counseling, delegating, recognizing, reporting, etc.

700

- Are the following duties assigned to different persons:

- Approval of each payroll,

- Processing and recording payroll,

- The reconciliation of related bank statements

- Possession of processed payroll checks

- Ability to enter or change employee bank account numbers

- Ability to add employees to the payroll system or to remove them

700

set of concepts

and principles that have come to be known as Generally Accepted Accounting Principles (GAAP)

Business entity concept. Every organization that operates separately is treated as a business under the business entity

concept. The purpose of accounting is to report each entity’s financial position on a balance sheet and its profitability on

an income statement. The employees, owners, and managers of a business entity must keep their personal transactions

separate from those of the business entity.

Continuing concern concept. This concept assumes a business entity will continue to operate indefinitely as a business.

If the business is for sale, it would not be a continuing concern and its assets would be valued at their fair market value.

Continuing concerns value their assets at their cost since they are not for sale.

Time period concept. Each organization must determine its own accounting period based on the type of business it is

engaged in. For its yearly accounting period, an organization can choose either the calendar year or another 12-month

period (fiscal year, e.g., June 1, 2018, to May 31, 2019). In most organizations, the end of the fiscal year coincides with

the least business activity for the year

Cost principle. Because organizations are assumed to continue as going concerns, all goods and services purchased

(assets) are recorded at the cost of acquiring them. The cost is measured by the cash spent or the cash equivalent of

goods or services provided in return for those purchased. Once valued, an asset remains at that value for its life minus

any depreciation in accordance with the continuing concern concept and the objectivity principle (see discussion

following).

Objectivity principle. Transactions must be recorded objectively to ensure personal opinions and emotions are not

part of the recorded transaction. This principle ensures accounting information will be useful for lenders and investors.

Generally, valuing an asset at cost meets this principle since it requires a deal between a buyer and a seller with different

goals in completing the transaction.

Matching principle. Expenses and revenue are recorded in the accounting period in which the expense is incurred or

the revenue is earned. Under the matching principle, transactions may have to be recorded before any money actually

changes hands, but after the essence of the transaction has been completed. The matching principle allows a comparison

between different organizations’ financial statements.

Realization principle. The realization principle governs the recording of revenue. Revenue is the income received for

goods and services provided by the organization. Revenue is recognized (or realized) and reported when earned, which

is during the accounting period when the goods have been transferred or the services provided. The amount recognized

is the cash received or the fair market value of goods and services received.

Consistency principle. Transactions must be recorded in a consistent manner based on the particular accounting

method, principle, or period. Users of accounting information require that transactions be recorded consistently so they

can make sound financial decisions regarding the organization, especially when comparing previous accounting periods

to the current period.

800

I9

Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding

800

McNamara-O’Hara

Service Contract Act379

applies to employers that contract with the federal government to

provide services to a federal agency. It applies to contracts over $2,500 and requires that employees be paid prevailing

minimum wages and fringe benefits based on the wages and benefits for similar employment in the locality or on a

collective bargaining agreement (the Secretary of Labor decides), but no less than the minimum wage under the FLSA.

800

Golden Parachute Payments

When companies change ownership, key executives are often provided with “golden parachutes” to soften their landing

should they be terminated by the new owner.

800

Enterprise Resource Planning (ERP) system features

Financial Operations

An ERP can automate, simplify and evaluate most accounting processes. What can take employees days to analyze and compute can be achieved within minutes using an ERP. An ERP can facilitate payroll, budgeting, billing and banking operations. The software can conduct cost analyses to better manage cash flow and forecast future growth. Using the ERP to perform these functions can reduce human error and help cut costs.

Human Resources

An ERP can not only help with hiring and training new employees, but also tracking their individual productivity. Each employee can log into the system and enter time worked and manage benefits and vacation time. The ERP can automate payroll processes, removing the need for an extensive payroll department. ERP software can send out employee surveys and news, provide an online community for employee collaboration and contain the policies and procedures for a company.

Production and Distribution

Some functionality included in an ERP that can benefit the manufacturing department by providing production control, process synchronization and quality evaluation. An ERP can also analyze the financials of a manufacturing company and automatically adjust processes based on cost analysis and forecasting. The software can automate distribution scheduling that often takes up precious employee time.

Orders and Inventory

What begins with the sales team needs to flow seamlessly to the inventory management team. Inventory and materials management helps companies keep track of stock, set appropriate price points and locate items within the warehouse. Supply chain management eliminates the human error that can result in costly mistakes in the distribution system.

800

most important decisions a payroll manager can make and consequences

whether to hire a

particular person. The stakes are high, since employees who perform well as enthusiastic team members can lead to an

efficient, cost-effective

payroll department, while hiring the wrong individuals can lead to dissension, inefficiency, and

costly turnover. As with any important task, hiring consists of more than one activity.

800

Primary Risks for Payroll

- Payroll is intentionally understated

- Inappropriate parties receive payments

- Employees receive duplicate payments

As you think about these risks, consider the control deficiencies that allow payroll misstatements.

800

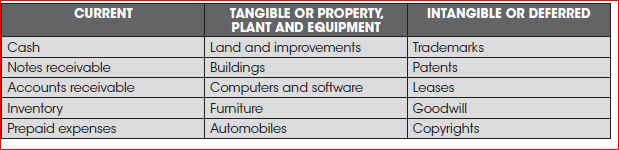

list of some of a typical company’s assets

900

SS4

Application for Employer Identification Number

(For use by employers, corporations, partnerships, trusts, estates, churches,

government agencies, Indian tribal entities, certain individuals, and others.)

▶ Go to www.irs.gov/FormSS4 for instructions and the latest information.

▶ See separate instructions for each line. ▶ Keep a copy for your records

900

The Contract Work Hours and Safety Standards Act

requires contractors with the federal government (not those

already covered by Walsh-Healey)

to pay employees overtime of at least 1½ times their “basic rate” for hours worked

over 40 in a workweek. Overtime must be paid only for work covered by the contract (Walsh-Healey

applies to both

covered and uncovered work). The law applies to contracts over $100,000.

The basic rate is the same as the employee’s regular rate under the FLSA. Violators are subject to liquidated damages of

$26 per day for each employee working in violation of the Act. Such amounts can be withheld from amounts owed the

contractor under its contract with the federal government.

900

Jury Duty Pay tax treatment

1. If the employer pays an employee his or her regular wages in addition to jury duty pay received from the

government unit involved, the wages are subject to federal income tax withholding and social security,

Medicare, and FUTA taxes.

2. If the employer pays an employee the difference between the employee’s regular pay and the jury duty pay,

only that difference is subject to federal income tax withholding and social security, Medicare, and FUTA

taxes.

3. If the employer pays an employee wages for time spent on jury duty but requires the employee to turn over

the jury duty pay to the employer, only the difference between the amount paid and amount turned over

is subject to federal income tax withholding and social security, Medicare, and FUTA taxes. The employee

may deduct the amount turned over on his or her personal income tax return.

900

Payroll System basics

• Pay Processing –based

on calculation formulas, process payroll on a predetermined basis and calculate and

maintain records for pension or retirement contributions

• Payroll Reporting –access

to payroll reports including tax reporting and analytics with built-in

templates

and parameter-driven

reporting configuration

• Check Printing –print

checks and provide employees electronic access to earnings statements

• Direct Deposit and Paycards –set

up direct deposit and paycard accounts or distribute funds to a combination

of a check and direct deposit/paycard accounts

• Retirement Plan Reporting –calculate

and report retirement plans using file formats for major retirement

plan providers or pension plans

• Garnishment Processing –deductions

based on disposable earnings or take home pay and legal

requirements

• Time and Attendance –an

automated system for gathering time data and processing it from “punch to

payroll”

In addition, there are some advanced features, functions, and services that may be required within a given organization

that should be identified:

• Compensation Planning and Management

• Global Database and Reporting

• Talent Acquisition and Management

• Learning and Development

900

Training import

It is important for the payroll manager to keep in mind just

what training can and cannot do. While training can improve performance, it is not a cure-all

for every performance

problem. Proper training can improve an employee’s knowledge and skills, improvements which they can then use to

bring their job performance up to standard or to prepare them for a new job or promotion. What training will not do

is improve an employee’s poor attitude or work ethic, problems that can possibly be resolved by disciplinary action or

counseling.

900

payroll control deficiencies:

- One person performs two or more of the following:

- Approves payroll payments to employees,

- Enters time or salary rates in the payroll system,

- Issues payroll checks or makes direct deposit payments,

- Adds or removes employees from the payroll system

- Reconciles the payroll bank account

- No one reviews and approves recorded time

- No one reviews and approves payroll before processing

- No one performs surprise audits of payroll

- Appropriate procedures for adding and removing employees are not present

- No one reviews the removal of terminated employees from payroll

- No one compares payroll expenses to a budget

900

Expense account examples

Wages paid to employees

• Employer-paid

benefit costs

• Maintenance for computers

• Office supply costs

• Employer share of payroll taxes

1000

W7

Application for IRS Individual

Taxpayer Identification Number

▶ For use by individuals who are not U.S. citizens or permanent residents.

▶ See separate instructions.

OMB No. 1545-0074

An IRS individual taxpayer identification number (ITIN) is for federal tax purposes only

1000

Copeland ‘Anti-Kickback’

Act

imposes fines and jail time on anyone who induces any employee

working on a federally financed construction, building, or public works project to give up or “kick back” any part of the

employee’s compensation to which the employee is entitled under a federal contract.380

Another portion requires the Secretary of Labor to issue regulations for federal construction and public works contractors

and subcontractors that require them to furnish a pay statement to their employees each week.

1000

Loans to Employees taxability

The taxable amount is not subject to federal income tax withholding, but must be reported on the employee’s Form

W-2.

The taxable amount is subject to social security, Medicare, and FUTA taxes. If the employer forgives the debt, or

for any other reason the employee is not expected to repay the loan, the entire balance of the loan becomes income subject

to federal income tax withholding and social security, Medicare, and FUTA taxes in the year the debt is forgiven.

1000

Project Team members should be

• Payroll

• Human Resources

• Benefits

• Account Payable

• Accounting

• Tax

• Risk or Compliance

• Budget/Finance

• Data Processing/IT/MIS/HRIS

• Senior Management

1000

common barriers to listening

• Distractions from phone calls, emails, texts, people walking by the office, other interruptions

• Tuning out by thinking about something else or faking attention

• Reacting emotionally rather than rationally

• Failing to pay attention to the speaker’s body language

• Not meaning what you say or saying what you mean when speaking

• Anticipating what you will say next without really listening

1000

Substantive Procedures for Payroll for auditing payroll

- Reconcile 941s to payroll

- Recompute accrued payroll liability (amount recorded at period-end)

- Review payroll withholding accounts for appropriateness and vouch subsequent payments for any significant amounts

- Compare payroll expenses (including benefits) to budget and examine any unexplained variances

- When control weaknesses are present, design and perform procedures to address the related risks

- Compare accrued vacation to prior periods and current payroll activity

1000

Liability account examples

• Income and employment taxes withheld but not yet deposited

• Contributions owed to a company benefit plan

• Accounts payable

• Wages payable

• Union dues deducted from pay but not yet paid to the union