CCC (Cost Curve Calc.)

The Golden Rule

Graphing, Graphing and More Graphing

Run, Forrest, Run!

Misc.

100

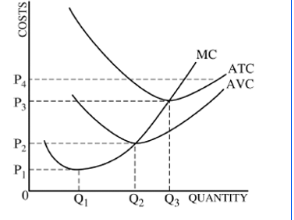

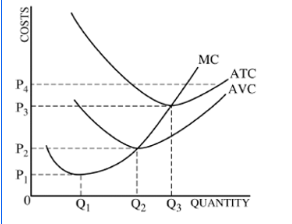

The AFC is $22 and the AVC is $31, the ATC must be this.

What is $53?

100

Profit maximization.

What is MR = MC?

100

The distance between ATC and AVC on a graph.

What is AFC?

100

Perfectly competitive firms make this in the long run.

What is zero economic profit?

100

Firms produce at this quantity.

What is MR = MC?

200

At 9 units, fixed cost is $20, variable cost is $79, Average total cost is __________.

What is $11?

200

A farmer produces corn in a perfectly competitive market. If the price falls, in the short run, the farmer should produce only if price covers this.

What is average variable cost?

200

If price is above _____, firms will enter the industry.

If price is above _____, firms will enter the industry.

What is P3?

200

Firms will do this if they see firms making a short run loss.

What is leave the market?

200

This would lead to zero economic profits.

What is free entry and exit of firms, perfectly elastic demand, many firms making identical products, etc.?

300

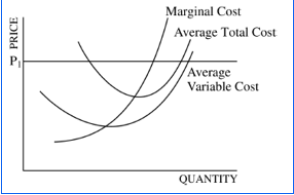

In the short run, if a firm produces the level of output at which marginal revenue is equal to marginal cost but price is less than average variable cost, the firm will do this.

What is shut down?

300

In perfect competition, firms will make a profit if this curve is below average revenue at the profit maximizing point.

What is ATC?

300

In the short run, firms will realize an economic loss but will continue to produce if the price is between these points.

In the short run, firms will realize an economic loss but will continue to produce if the price is between these points.

What are P2 and P3?

300

Area of profit or loss is shaded between these two points, with the profit maximizing quantity being the right edge.

What are cost per unit (ATC @ profit maximizing quantity) and price?

300

Demand for perfectly competitive firms in the short run is this.

What is perfectly elastic?

400

Average variable cost will equal this if fixed cost is zero.

What is average total cost?

400

Productive efficiency occurs when a firm produces output at this level.

What is when average total cost is at a minimum?

400

Firms will do this if they see firms making this in the short run.

Firms will do this if they see firms making this in the short run.

What is enter the market?

400

Pencil producers are experiencing short run profit. This will happen to equilibrium price and quantity of pencils in the long run. (explain why)

What is firms will enter the market, causing supply to shift right; the rightward shift causes quantity to go up and price to go down until long run economic profit = 0?

400

A downward sloping long run average total cost curve is caused by this.

What is increasing returns to scale? (note: the question is describing economies of scale; economies of scale itself is when the ATC is downward sloping, increasing returns to scale is what causes this.)

500

At 354 units of output, the firm's total cost is $6500. The firm's total fixed cost is $1250, making average variable cost this.

What is $14.83?

500

Marginal cost equals AVC at 12 dollars, marginal cost equals ATC at 17 dollars, and marginal revenue equals marginal cost at 14 dollars, the firm will do this.

What is operate in the short run sustaining a loss?

500

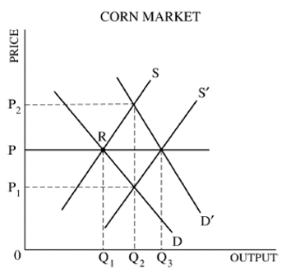

Assume that the corn market is initially in long-run equilibrium at point R. The short-run and long-run prices of corn if more corn is used as a source of alternative energy, are these points.

What is short run P2, long run P?

500

Gibson Guitars are produced in a perfectly competitive market. Famous economics teacher Mr. Verdico is seen playing a Gibson Guitar. The market price and quantity of Gibson guitars do this in the short run, and an individual Gibson guitar producer will experience this in the short run.

What is equilibrium price and quantity will increase (due to an increase in demand) and an individual producer will see a profit?

500

When trying to find cost per unit to determine if firms are making a short run profit or loss, you find this curve at the profit maximizing quantity.

What is average total cost?