Demand

Supply

Supply and Demand

PPC

Hodgepodge

100

if price increases quantity demanded will go down

law of demand

100

if price increases then the quantity supplied will increase

law of supply

100

The point where supply and demand meet; tells us the proper price and quantity to be efficient

Equilibrium

100

What does PPC stand for?

Production Possibilities Curve

100

The latin phrase that means "All other things being unchanged"

Ceteris Paribus

200

Slope of demand curve

downward

200

Price's relationship to Quantity Supplied

DIRECT

(One goes up, so does the other)

200

The workers who produce batteries go on strike.

Shift in Supply or Demand? Increase or Decrease

Supply Decreases

200

On the "curve"

Efficient

200

What are the FOUR FACTORS of Production

Land, Labor, Capital, and Entrepreneurship

300

The numeric (table) representation of a Demand Function

demand schedule

300

The expected effect on the market if there were a decrease in the cost of an input.

Increase (right shift) in supply

300

The price of wheat and corn, key resources in the production of cereal decreases.

Supply or Demand, Increase or Decrease, and what is the SHIFTER?

Supply, Increase, Price of RESOURCES

300

In a two product economy, a CONSTANT opportunity cost will appear as this type of Production Possibility Curve.

Linear

300

having a lower opportunity cost for a good gives a producer this

comparative advantage

400

The effect of a personal tax increase in a market (Not a business tax... i.e. People's own individual taxes go up)

decrease (left shift) in demand

(Taxes reduce people's INCOME)

400

The spread of a damaging computer virus would have this effect on the power generation market.

decrease in supply

400

If the price of a good is set too high (Either by a price floor or just choices of producers) it will create this situation.

A Surplus of the good

400

Outside the "curve"

unattainable

400

Soccer balls and basketballs are substitutes. An increase in basketball prices would have this effect on the soccer ball market.

increase in demand

500

Difference between substitute good and complimentary good

-Substitute goods are competitors and have opposite reaction to price changes

-Complimentary goods are used together and have same reaction to price changes.

500

Product A is an input to Product B which is a substitute for Product C.

An increase in the price of Product A has this effect on Product B.

decrease in supply

*shift left*

500

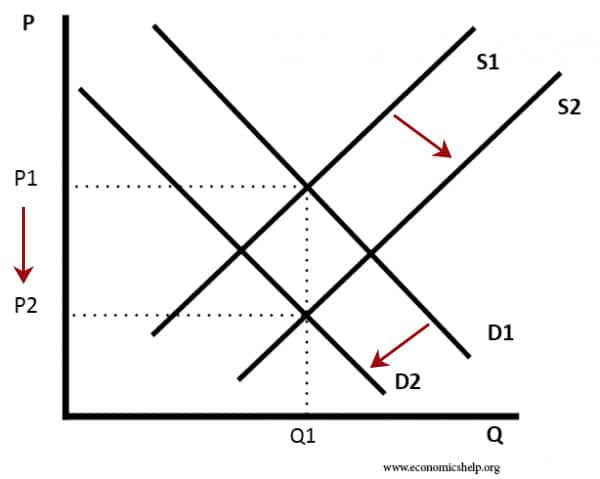

The change in equilibrium price and quantity resulting from a simultaneous increase in supply AND a decrease in demand

PRICE definitely decrease

Quantity is uncertain

500

Concepts represented on a PPC

Scarcity

Choice

Efficiency

Inefficiency

500

France Bushels of Grapes 100

France Bushels of Tomatoes 25

Italy Bushels of Grapes 100

Italy Bushels of Tomatoes 50

(a) Does France, Italy, or neither nation have a comparative advantage in producing grapes? Explain.

France has a comparative advantage in producing grapes and explains that France’s opportunity cost of producing 1 bushel of grapes (0.25 of a bushel of tomatoes) is less than Italy’s opportunity cost of producing 1 bushel of grapes (0.5 of a bushel of tomatoes).

[France’s opportunity cost of producing 1 bushel of grapes is 0.25 of a bushel of tomatoes (25/100 = 0.25)(25/100 = 0.25) . Italy’s opportunity cost of producing 1 bushel of grapes is 0.5 of a bushel of tomatoes (50/100 = 0.5)