#1

#2

#3

#4

#5

100

Scarcity is best defined as

A. the difference between limited wants and limited economic resources.

B. the difference between the total benefit of an action and the total cost of that action.

C. the difference between unlimited wants and limited economic resources.

D. the opportunity cost of pursuing a given course of action.

E. the difference between the marginal benefit and marginal cost of an action.

C. the difference between unlimited wants and limited economic resources.

100

If the demand for grapes increases simultaneously with an increase in the supply of grapes, we can say that

A. equilibrium quantity rises, but the price change is ambiguous.

B. equilibrium quantity falls, but the price change is ambiguous.

C. equilibrium quantity rises, and the price rises.

D. equilibrium quantity falls, and the price falls.

E. the quantity change is ambiguous, but the equilibrium price rises.

A. equilibrium quantity rises, but the price change is ambiguous.

100

Monopolistic competition is often characterized by

A. strong barriers to entry.

B. a long-run price that exceeds average total cost.

C. a price that exceeds average variable cost, causing excess capacity.

D. a homogenous product.

E. many resources devoted to advertising.

E. many resources devoted to advertising.

100

Which of the following will increase wages for tuba makers?

A. An increase in the number of graduates at tuba maker training school

B. An increase in the price of tubas

C. An increase in the price of tuba lessons

D. An increase in the tax on tubas

E. An effective price ceiling for tubas

B. An increase in the price of tubas

100

Which of the following are associated with public goods?

I. Free riders

II. Adding demand curves vertically to find the demand curve for society

III. Nonrivalry in consumption

IV. Nonexcludability

A. I and II only

B. I and IV only

C. II and III only

D. I, III, and IV only

E. I, II, III, and IV

E. I, II, III, and IV

200

Which of the following statements is most consistent with a capitalist market economy?

A. Economic resources are allocated according to the decisions of the central bank.

B. Private property is fundamental to innovation, growth, and trade.

C. A central government plans the production and distribution of goods.

D. Most wages and prices are legally controlled.

E. Most economic resources are owned by the government and leased to the citizens in exchange for lower taxes.

B. Private property is fundamental to innovation, growth, and trade.

200

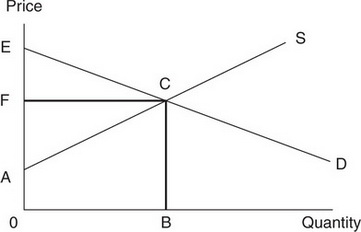

In Figure above, identify the area of consumer surplus.

A. 0ACB

B. 0FCB

C. AFC

D. ACE

E. FCE

E. FCE

200

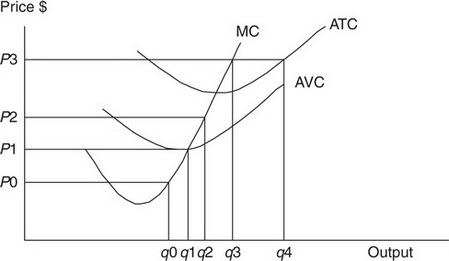

The Figure below illustrates the short-run cost curves of a perfectly competitive firm.

The shutdown point is seen at:

A. P0, q0

B. P1, q1

C. P2, q2

D. P3, q3

E. P3, q4

Correct Answer: B

B-The shutdown point is at minimum AVC. If the price falls below this point, the firm finds it rational to produce nothing in the short run and incur losses equal to TFC.

200

When the opportunity for price discrimination arises,

A. market segments with relatively elastic demand pay higher prices

B. market segments with relatively inelastic demand pay lower prices

C. consumer surplus decreases

D. demand is horizontal

E. demand is vertical

C. consumer surplus decreases

200

12. Which of the following statements about a price ceiling is accurate?

A. An effective price ceiling must be at a price below the equilibrium price.

B. A price ceiling will increase the quantity of the good supplied.

C. A price ceiling will cause a shift in the demand curve for the good.

D. A price ceiling will have no effect on the quantity of the good supplied.

E. Surpluses in the supply of the good are among the results of a price ceiling.

A. An effective price ceiling must be at a price below the equilibrium price.

300

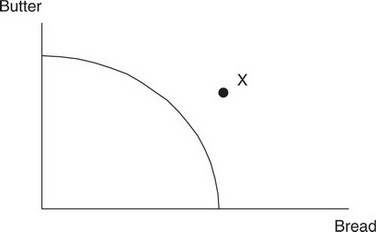

The graph in Figure above shows a nation's production possibility curve (PPC) for the production of bread and butter. Which of the following is true?

A. The opportunity cost of producing more butter is a decreasing amount of bread.

B. Point X represents unemployed economic resources.

C. The opportunity cost of producing more butter is a constant amount of bread.

D. Point X represents a labor force that has become less productive.

E. The opportunity cost of producing more butter is an increasing amount of bread.

E. The opportunity cost of producing more butter is an increasing amount of bread.

300

8. Suppose the price of beef rises by 10 percent and the quantity of beef demanded falls by 20 percent. We can conclude that

A. demand for beef is price elastic and consumer spending on beef is falling.

B. demand for beef is price elastic and consumer spending on beef is rising.

C. demand for beef is price inelastic and consumer spending on beef is falling.

D. demand for beef is price inelastic and consumer spending on beef is rising.

E. demand for beef is unit elastic and consumer spending on beef is constant.

A. demand for beef is price elastic and consumer spending on beef is falling.

300

The Figure below illustrates the short-run cost curves of a perfectly competitive firm.

If the market price of the output increases from P1 to P3, the profit-maximizing firm will

A. increase output from q1 to q4 and earn positive economic profits.

B. increase output from q1 to q4 and earn a normal profit.

C. increase output from q1 to q3 and earn positive economic profits.

D. increase output from q1 to q3 and earn a normal profit.

E. increase output from q1 to q2 and earn economic losses.

C. increase output from q1 to q3 and earn positive economic profits.

300

When a perfectly competitive labor market is in equilibrium,

A. everyone who wants to work has the opportunity to do so

B. individual firms face downward sloping labor demand curves

C. unemployment can reach as high as 10-15 percent

D. individual firms face upward sloping labor demand curves

E. individual firms are considered "price makers"

A. everyone who wants to work has the opportunity to do so

300

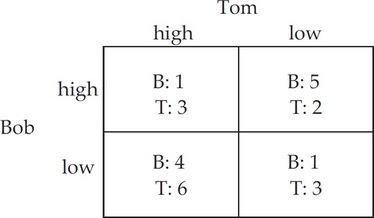

In the payoff matrix in the figure, a dominant strategy equilibrium

A. is for Bob to go high and Tom to go low

B. is for both Bob and Tom to go low

C. is for Bob to go low and Tom to go high

D. is for both Bob and Tom to go high

E. does not exist

E. does not exist

E Dominant strategies, dominant strategy equilibria, and Nash equilibria are easily found using the "circle" method explained in the game theory section of this book. Briefly, for each possible strategy for Bob, you circle the payoff for the best move for Tom and vice versa. If Tom has two payoffs circled in the same column (or row if you put him on the left rather than the top) as he does in the "high" column, then "high" is a dominant strategy for Tom—he should do it regardless of what Bob does. If Bob has two payoffs circled in the same row (or column if he's on top) then the strategy represented by that row is dominant for Bob. A dominant strategy equilibrium exists when both players have a dominant strategy. The box with two circles in it indicates the dominant strategy equilibrium if it exists. However, because Bob should go high if Tom goes low and Bob should go low if Tom goes high, Bob does not have a dominant strategy and a dominant strategy equilibrium does not exist.

400

4. Which of the following is true of equilibrium in a purely (or perfectly) competitive market for good X?

A. A shortage of good X exists.

B. The quantity demanded equals the quantity supplied of good X.

C. A surplus of good X exists.

D. The government regulates the quantity of good X produced at the market price.

E. Deadweight loss exists.

B. The quantity demanded equals the quantity supplied of good X.

400

If the price of firm A's cell phone service rises by 5 percent and the quantity demanded for firm B's cell phone service increases by 10 percent, we can say that

A. demand for firm B is price elastic.

B. supply for firm B is price elastic.

C. firms A and B are substitutes because the cross-price elasticity is greater than zero.

D. firms A and B are complements because the cross-price elasticity is less than zero.

E. firms A and B are complements because the cross-price elasticity is greater than zero.

C. firms A and B are substitutes because the cross-price elasticity is greater than zero.

400

Every time Mr. Hamm makes another pizza in his shop, he places $0.45 worth of sauce on top. For Mr. Hamm, the cost of pizza sauce is a component of which of the following?

I. Total Fixed Costs

II. Total Variable Costs

III. Marginal Cost

IV. Total Costs

A. I and IV only

B. II and III only

C. II and IV only

D. III and IV only

E. II, III, and IV only

E. II, III, and IV only

400

A production possibility frontier will be a straight line when

A. efficiency is achieved

B. the goods on the axes are perfect substitutes in consumption

C. utility is maximized

D. resources are not specialized

E. the marginal product functions for all inputs are straight lines

D. resources are not specialized

400

In the long run, a monopolistically competitive firm

A. earns zero economic profit

B. earns positive economic profit

C. earns negative economic profit

D. faces a vertical demand curve

E. faces a horizontal demand curve

A. earns zero economic profit

500

5. The competitive market for gasoline, a normal good, is currently in a state of equilibrium. Which of the following would most likely increase the price of gasoline?

A. Household income falls.

B. Technology used to produce gasoline improves.

C. The price of subway tickets and other public transportation falls.

D. The price of crude oil, a raw material for gasoline, rises.

E. The price of car insurance rises.

D. The price of crude oil, a raw material for gasoline, rises.

500

Which of the following describes the theory behind the demand curve?

A. Decreasing marginal utility as consumption rises.

B. Increasing marginal cost as consumption rises.

C. Decreasing marginal cost as consumption rises.

D. Increasing total utility at an increasing rate as consumption rises.

E. The substitution effect is larger than the income effect.

A. Decreasing marginal utility as consumption rises.

500

If the government wants to establish a socially optimal price for a natural monopoly, it should select the price at which

A. average revenue equals zero

B. marginal revenue equals zero

C. the marginal cost curve intersects the demand curve

D. the average total cost curve intersects the demand curve

E. marginal revenue equals marginal cost

C. the marginal cost curve intersects the demand curve

500

An industry with three firms selling a standardized or differentiated product would be called

A. a competitive industry

B. a monopolistically competitive industry

C. an oligopoly

D. a duopoly

E. a monopoly

E. a monopoly

500

Which of the following is most likely to result in a shift to the right in the demand curve for orange juice?

A. A bumper crop of oranges in Florida

B. A decrease in the price of Tang

C. Expectations of lower future prices for orange juice

D. A law permitting orange pickers to be paid less than the minimum wage

E. Expectations of higher future income among juice drinkers

E. Expectations of higher future income among juice drinkers