Decedent Final Tax Return

Estates & Trusts

Farmers

Exempt Organizations

Rental Property

100

Income in respect of a decedent must not be included in the income of which of the following?

- The decedent's final Form 1040 filing

- The decedent's estate (if received by the estate)

- The beneficiary's filing (if the right to income is passed directly to and received by the beneficiary)

- Any person to whom the estate properly distributes the right to receive it

The decedent's final Form 1040 filing

The decedent's income includible on the final return is generally determined as if the person were still alive except that the taxable period is usually shorter because it ends on the date of death. All income the decedent would have received had death not occurred that was not properly includible on the final return is income in respect of a decedent (IRD). The final return does not include IRD.

100

Anissa's father died in February 20X1. Anissa is the sole beneficiary of her father's estate. The estate was closed December 20X1 and the executor is filing one (first and final) Form 1041. After all expenses of the estate were paid, the following amounts were paid out to Anissa in 20X1:

- Cash $12,000

- IRA distribution of $300,000 (decedent had no basis)

- Wages paid after death $6,000

- Stock $75,000

- Life insurance $150,000

How much, if any, of the amounts paid, will be reported on Anissa's 20X1 Form 1040 income tax return?

- $0

- $6,000

- $306,000

- $543,000

$306,000

Certain types of property, such as capital assets, receive a step-up in basis when included in the decedent's estate and transferred to a beneficiary due to death. Life insurance proceeds are generally tax-free to the beneficiary. Other assets, for example, traditional IRA's, are transferred in-kind to the beneficiary and do not receive a basis adjustment. The income and growth within these accounts that have not been taxed, is subject to tax upon receipt by the beneficiary. All income the decedent would have received had death not occurred that was not properly includible on the final return is income in respect of a decedent (IRD).

The estate is the beneficiary of the IRA, not Anissa. If Anissa were the named beneficiary, the IRA would not be part of the probate estate. The IRA must be withdrawn by an estate within 5 years, but if handled properly the executor can direct the custodian to establish an inherited IRA for the benefit of Anissa. Unfortunately for Anissa, the amount held in the IRA was distributed so she must pay taxes on the entire amount of IRD along with the wages paid after death.

100

Farmer Judy is a calendar-year taxpayer who uses the cash method of accounting. She normally sells 200 head of sheep a year. Because of a drought, she sold 250 head of sheep in 20X1. Farmer Judy realized $50,000 from the sale. The affected area was declared a disaster area eligible for federal assistance on March 12, 20X1. How much, if any, income can Farmer Judy postpone to 20X2?

- $10,000

- $50,000

- $12,500

- $0, since only sales because of flooding qualify for postponement

$10,000

If you sell or exchange more livestock (including sheep) than you normally would in a year because of a drought, flood, or other weather-related condition, you may be able to postpone reporting the gain from the additional animals until the next year. Judy sold 50 more head of sheep than normal so she may defer $10,000 (50 ÷ 250 × $50,000).

100

An organization may qualify under Section 501(c)(3) if it is organized exclusively for which of the following purposes?

- charitable

- business

- political action

- personal

Charitable

An organization may qualify for exemption from federal income tax if it is organized and operated exclusively for one or more of the following purposes:

- Religious

- Charitable

- Scientific

- Testing for public safety

- Literary

- Educational (includes public daycare for children to enable parents to work)

- Fostering national or international amateur sports competition (but only if none of its activities involve providing athletic facilities or equipment)

- The prevention of cruelty to children or animals

Form 1023; Code Section 501(c)(3)

100

Kathy rented out her summer home for 80 days plus used it personally for 20 days. She paid $1,000 for repairs and $2,000 for utilities. Rental income was $8,000. What was Kathy's net rental income?

- $0

- $5,000

- $5,600

- $8,000

$5,600

Because Kathy uses the property more than 10% of the time, she must allocate expenses between rental and personal use. If 80% of the use is rented out at fair market rental rates, she can deduct 80% of the expenses from her rental income. Total expense of $3,000 × 80% = $2,400. Gross rental income of $8,000 – $2,400 of allowable expenses = $5,600 net rental income.

200

Review the list of tax credits below.

- Earned Income Credit

- Child Tax Credit

- Saver’s Credit

- American Opportunity Tax Credit

Which of the credits listed above may a decedent claim on their final income tax return, assuming they met all eligibility requirements for the tax year prior to death?

- I and II

- III

- II, III and IV

- I, II, III and IV

I, II, III and IV

The individual filing a decedent’s tax return may claim any tax credits that applied to the decedent before death on the decedent’s final income tax return. Certain credits, like the EIC or the child tax credit, still apply even though the return covers a period of fewer than 12 months.

200

The John Q estate fiscal tax year runs from April 1, 20X1, to March 31, 20X2. The estate made distributions to beneficiaries on December 12, 20X1, and March 15, 20X2. Assuming the estate has taxable income, in what year(s) tax return(s) will its beneficiaries be required to report taxable distributions on?

- 20X1

- 20X2

- Both 20X1 and 20X2

- Neither 20X1 nor 20X2

20X2

Beneficiaries must include their share of the estate income on the return for the tax year in which the last day of the estate's tax year falls. Since the last day of the estate's tax year is March 31, 20X2, all income received by the beneficiaries from the estate between April 1, 20X1 and March 31, 20X2, must be reported on their 20X2 income tax return

200

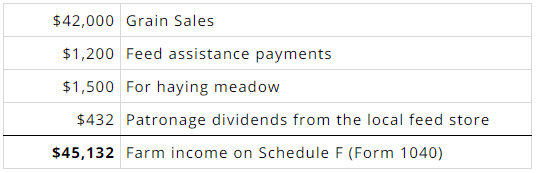

Leonard Brown operated a cattle and grain farm in 20X1. Leonard sold $42,000 of grain and $23,000 of cattle held for breeding purposes. Leonard also received patronage dividends from the local feed store of $432, feed assistance payments of $1,200, and $1,500 for haying a neighbor's meadow. Leonard should report the following on Schedule F of his federal income tax return for 20X1:

- $45,132

- $67,700

- $44,700

- $66,932

$45,132

Farmers use Schedule F (Form 1040) to figure the net profit or loss from regular farming operations. Income from farming reported on Schedule F includes amounts from cultivating, operating, or managing a farm for gain or profit, either as owner or tenant. This includes income from operating stock, dairy, poultry, fish, fruit, or truck farm and income from operating a plantation, ranch, range, or orchard. It also includes income from the sale of crop shares if you materially participate in producing the crop.

Sales of livestock used in the business (not held for resale), for draft, breeding, sport, or dairy purposes result in ordinary or capital gains or losses, depending on the circumstances. In general, this is reported on Form 4797.

200

A small university which operates as a private not-for-profit organization has received tax exempt status from the Internal Revenue Service. Thus, the charity gets to use a nonprofit postal permit for its mailings which reduces its costs significantly. In addition, except for unrelated business income, the charity pays no federal income taxes. Gifts made to the organization are tax deductible by the donor. What is the label that is attached to this tax exempt status?

- Section 501 (c) (1)

- Section 501 (c) (3)

- Section 501 (c) (4)

- Section 501 (c) (6)

Section 501 (c) (3)

Not-for-profit organizations that are charitable, educational, or scientific typically operate as Section 501 (c) (3) tax-exempt organizations and receive the benefits mentioned. Organizations created under acts of Congress (such as Federal Credit Unions) are identified as Section 501 (c) (1) organizations. Political advocacy groups can qualify as Section 501 (c) (4) organizations although donations are not tax deductible for the donor. Business leagues, chambers of commerce, and the like are Section 501 (c) (6). Section 501 (c) (3) is the most widely mentioned of these tax-exempt classifications because of the number of organizations that qualify and because of the significant benefits.

200

During the current year, Bob rented out his condominium for 10 days when the local NASCAR races were in town. Bob used the condo himself for a total of 75 days during the year. Revenue for the 10 rental days was $2,500. Expenses for the condo for the year were $6,000 in property taxes and $600 for utilities. What amount of the rental income is includable in Bob's taxable income?

- None

- $2,301

- $2,465

- $2,500

None

Since the property was rented out for less than 15 days, no rental income is includable and expenses attributable to the rental are not deductible. The property taxes are still deductible in full on Schedule A.

300

The decedent died on June 30. The decedent used the cash method of accounting and a calendar year-end. What total amount of the following is includible in the decedent's final return (Form 1040)? Total received during the tax year $5,000:

- Taxable Interest (earned and received equally all year) $2,000

- Dividends (declared on June 15 and received on July 10) $500

- Final wages (received July 10) $2,500

- $1,000

- $2,500

- $4,000

- $3,500

$1,000

If the decedent accounted for income under the cash method, only those items actually or constructively received before death are included in the final return. Half of the interest had been earned and received as of date of death, so $1,000 of it is reported on the decedent's final return. The wages were not constructively received until July 10th, and are not included on the final return. The same is true for the dividends. If the individual died between the time the corporation declared the dividend and the time it arrived in the mail, the decedent did not constructively receive it before death. Do not include the dividend in the final return. All income the decedent would have received had death not occurred that was not properly includible on the decedent's final return, is income in respect of a decedent (IRD). Income in respect of a decedent is included in the income of one of the following:

- The decedent's estate, if the estate receives it

- The beneficiary, if the right to income is passed directly to the beneficiary and the beneficiary receives it

- Any person to whom the estate properly distributes the right to receive it

300

The trustee of a grantor type trust must never:

- Give all payers of income the name and TIN of the grantor and the address of the trust

- File a trust return, completing only the entity information, and attach a statement identifying the grantor to whom the income is taxable

- File Forms 1099 with the IRS showing the trust income as paid to the grantor

- File a trust return, figuring the tax on all income and deductions of the trust

File a trust return, figuring the tax on all income and deductions of the trust

A grantor trust is a trust in which the grantor retains control and has an interest as beneficiary. Income from a grantor trust is taxed to the grantor as if no trust existed. Therefore, the trustee of a grantor trust would not file a trust return, figuring the tax on all income and deductions of the trust.

300

Who of the following may use farm income averaging, assuming farm income rules are met?

- A partner in a partnership engaged in a farming or fishing business, and a shareholder in an S Corporation engaged in a farming or fishing business.

- A partnership engaged in a farming or fishing business, an S Corporation engaged in a farming or fishing business, and a C Corporation engaged in a farming or fishing business.

- A partner in a partnership engaged in a farming or fishing business, and a shareholder in a C Corporation engaged in a farming or fishing business.

- A partner in a partnership engaged in a farming or fishing business, an estate engaged in a farming or fishing business, and a trust engaged in a farming or fishing business.

A partner in a partnership engaged in a farming or fishing business, and a shareholder in an S Corporation engaged in a farming or fishing business.

A taxpayer can use income averaging to figure tax for any year engaged in a farming business as an individual, a partner in a partnership, or a shareholder in an S corporation. Corporations, partnerships, S corporations, estates, and trusts cannot use income averaging.

300

The Haskins Society is a tax-exempt organization. Which of the following statements is not true about tax-exempt organizations?

- Unless the organization is a church or very small, it must officially file in order to gain tax exempt status.

- Unless the organization is a church or very small, it must file an annual informational return for tax purposes.

- If an organization is tax-exempt, then donations that it accepts can be taken as itemized deductions by the individuals making the gift.

- Even with a tax-exempt organization, unrelated business income above a certain level is still subject to income taxation.

If an organization is tax-exempt, then donations that it accepts can be taken as itemized deductions by the individuals making the gift

Regardless of their mission and intent, an organization (unless a church, or very small organization with gross annual receipts not more than $5,000) cannot simply assume that it has tax-exempt status. It must file Form 1023 by the end of 27 months from the end of the month of the organization's inception to gain that status and must then file an annual form (Form 990) to provide ongoing information.

Being tax-exempt does not keep the organization from having to pay income taxes if it generates unrelated business income over a maximum dollar limit ($1,000 in recent years).

Finally, being tax-exempt does allow donors to take a gift as a tax deduction but only in certain cases. For example, a Section 501(c)(3) tax-exempt organization (created for charitable, educational, or scientific purposes) offers this benefit. In contrast, a gift to a Section 501(c)(4) tax-exempt organization (an advocacy group) cannot be claimed by the donor as an itemized deduction.

300

Jose started renting a house to Bill for $600 per month beginning February 1, 20X1. Bill paid $1,200 on January 15, 20X1, which included the first month's rent and one month's security deposit. The rent is due by the 5th of the month. The lease specifies that the security deposit would also be used as the final month's rent. Bill pays the rent on the 2nd of each month. In July, Bill also paid $150 for repairs to the air conditioning system and in September he paid $80 for a roof repair. He deducted the amounts from the rent paid to Jose for those months. Bill was unable to pay December's rent until January of the next year. How much should Jose report as rental income for 20X1?

- $6,000

- $6,600

- $6,900

- $7,200

$6,600

If the tenant will use their security deposit as a final payment of rent, it is advance rent. The property owner should include it as income when received. Rental income includes expenses of the property owner paid by the tenant. Jose received 2 months worth of rent on Jan 15 (first and last month), and 9 more months through Nov 2, for a total of 11 payments. 11 months × $600 per month = $6,600 received in 20X1. Rent is reported as rental income in the year received.

400

The date of death plays a significant role in the treatment of income or expenses related to a deceased taxpayer. Which of the following statements about the final income tax return of the decedent is NOT true?

- Medical expenses paid for the decedent, decedent’s spouse, and dependents are deductible as itemized deductions on the final income tax return if the expenses were paid before death.

- A deceased taxpayer is eligible to claim any credits on the final income tax return that they could have claimed had they not died, including the EIC.

- A net operating loss deduction from a prior year can be deducted on the final income tax return.

- NOL or capital losses not used on the final income tax return can be carried over for deduction on the estate’s income tax return.

NOL or capital losses not used on the final income tax return can be carried over for deduction on the estate’s income tax return.

The correct answer to this question is the statement that is false. A decedent’s net operating loss deduction from a prior year and any capital losses (including capital loss carryovers) can be deducted only on the decedent’s final income tax return. An unused NOL or capital loss is not deductible on the estate’s income tax return.

400

The Bob Trust is a Simple Trust. Per the information listed below, how much taxable income is passed through to the beneficiaries?

- Taxable interest $1,000

- Tax-exempt interest $1,000

- Fiduciary fee $400

- $1,600

- $600

- $800

- $1,800

$800

The amount of taxable income that passes through to beneficiaries is $800 ($1,000 taxable interest – $200 fiduciary fee).

26 CFR 1.652(b)-3 (b) The deductions which are not directly attributable to a specific class of income may be allocated to any item of income (including capital gains) included in computing distributable net income, but a portion must be allocated to nontaxable income.

The income of a trust is $2,000, consisting equally of $1,000 of taxable interest and $1,000 tax-exempt interest. The fiduciary fee is applicable to all trust income, not a single class. The fiduciary fee is $400, but a portion of the fee must allocate to tax-exempt interest. This amount is 50% ($200) since tax-exempt interest represents one-half of all income included in DNI. The balance of $200 is allocated to taxable interest.

400

Farmer John, a cash basis farmer, operates a cow-calf breeding operation. The breeder cows are NOT primarily held for sale. In addition to the calves raised on his farm, John also purchases calves for resale. During 20X1, John had the following acquisitions and dispositions of cattle:

- Purchase of 30 calves for resale $3,420

- Sale of 30 calves purchased for resale $6,100

- Sale of 45 calves raised by John $10,400

- Sale of 10 breeder cows $6,750

- Original cost of breeder cows $5,500

- Accumulated depreciation on breeder cows $2,860

What amount should John include in gross income on his Schedule F for 20X1?

- $13,080

- $15,720

- $16,500

- $18,580

$13,080

Gain on the sale of raised livestock is generally the gross sales price reduced by any expenses of the sale. Expenses of sale include sales commissions, freight or hauling, and other similar expenses. The basis of the animal sold is zero if the farmer deducts the costs of raising it. Gain on the sale of purchased livestock is generally the gross sales price minus the adjusted basis and any expenses.

Sales of livestock used in the business (not held for resale), for draft, breeding, sport, or dairy purposes result in ordinary or capital gains or losses, depending on the circumstances. In general, this is reported on Form 4797, not Schedule F.

400

Which return might a tax-exempt organization be required to file?

- Employment tax returns.

- Annual information return, Form 990.

- Report of cash received.

- All of the above

All of the above

A tax-exempt organization may be required to file annual Information returns, employment tax returns, and a report of cash received.

400

John offers his beach cottage for rent from June through August 31 (92 days). His family uses the cottage during the last 2 weeks in May (15 days). He was unable to find a renter for the first week in August (7 days). The person who rented the cottage for July allowed him to use it over a weekend (2 days) without any reduction in or refund of rent. The cottage was not used at all before May 16th or after August 31st. Total income received was $11,000. Total expenses were $4,000. What percentage of the expenses for the cottage can John deduct as rental expenses?

- 25%

- 83%

- 85%

- 100%

85%

You figure the part of the cottage expenses to treat as rental expenses as follows:

- The cottage was used for rental a total of 85 days (92 – 7). The days it was available for rent but not rented (7 days) are not days of rental use. The July weekend (2 days) is rental use because John received a fair rental price for the weekend.

- John used the cottage for personal purposes for 15 days (the last 2 weeks in May).

- The total use of the cottage was 100 days (15 days personal use + 85 days rental use).

- The rental expenses are 85/100 (85%) of the cottage expenses.

500

John, a self-employed carpenter, died on January 8. Which of the following, if allowable, could be deducted on John's final Form 1040?

- Unused net operating loss carryover from prior year

- The full amount of his standard deduction (without proration)

- Medical expenses paid by the estate within one year of death

- All of the above

All of the above

All of the listed items can be used on the final Form 1040 if allowable. Any amounts not used are forfeited.

The amount of the standard deduction for a decedent's final tax return is the same as it would have been had the decedent continued to live. However, if the decedent was not 65 or older at the time of death, the higher standard deduction for age cannot be claimed.

If medical expenses are paid by the Estate within one year from the date of death an election can be made to deduct the expenses on the decedent's final individual tax return.

500

Given the following information, what is the distributable net income for the simple trust established by Mr. Bill?

- Dividend Income $20,000

- Taxable Interest Income $25,000

- Tax-Exempt Interest Income $10,000

- Long-Term Capital Gains $20,000 (Capital Gains are allocable to Corpus)

- Fiduciary Fees $5,000

- $70,000

- $60,000

- $50,000

- $40,000

$50,000

Exclude gains from the sale or exchange of capital assets from distributable net income (DNI) to the extent that such gains are allocated to corpus (trust principal) and are not paid, credited, or required to be distributed to any beneficiary during the taxable year. A simple trust is one that is required to distribute all income (not principal) currently.

DNI of the trust is the sum of interest and dividends income (taxable and tax-exempt) minus the fiduciary fee. Since the long-term capital gains are allocable to corpus, they are excluded from the DNI calculation.

DNI is $50,000 ($20,000 dividend income + $25,000 taxable interest income + $10,000 tax-exempt interest income – $5,000 fiduciary fee).

26 CFR 1.652(b)-3 (b)

The deductions which are not directly attributable to a specific class of income may be allocated to any item of income (including capital gains) included in computing distributable net income, but a portion must be allocated to nontaxable income (except dividends excluded under section 116) pursuant to section 265 and the regulations thereunder. For example, if the income of a trust is $30,000 (after direct expenses), consisting equally of $10,000 of dividends, tax-exempt interest, and rents, and income commissions amount to $3,000, one-third ($1,000) of such commissions should be allocated to tax-exempt interest, but the balance of $2,000 may be allocated to the rents or dividends in such proportions as the trustee may elect. The fact that the governing instrument or applicable local law treats certain items of deduction as attributable to corpus or to income not included in distributable net income does not affect allocation under this paragraph. For instance, if in the example set forth in this paragraph the trust also had capital gains which are allocable to corpus under the terms of the trust instrument, no part of the deductions would be allocable thereto since the capital gains are excluded from the computation of distributable net income under section 643(a)(3).

500

Which of the following statements is correct about crop insurance and disaster payments?

- The insurance proceeds can be deferred only if the farmer can show that the income from the crops would normally be reported in a tax year following the year of damage

- An accrual basis taxpayer can elect to include crop insurance proceeds in income for the tax year following the tax year in which the crops were damaged

- Insurance proceeds received in the tax year following the tax year in which the crops were destroyed can be deferred until the tax year following receipt of the proceeds

- A separate election to defer the inclusion of crop disaster payments must be made for each damaged crop of the trade or business

The insurance proceeds can be deferred only if the farmer can show that the income from the crops would normally be reported in a tax year following the year of damage

Farmers must include in income any crop insurance proceeds they receive as the result of crop damage. The income is generally recognized in the year received. Farmers can postpone reporting crop insurance proceeds as income until the year following the year the damage occurred if they meet all the following conditions:

- They use the cash method of accounting.

- They receive the crop insurance proceeds in the same tax year the crops are damaged.

- Under normal business practices, they would have included income from the damaged crops in any tax year following the year the damage occurred.

500

Which of the following organizations is not required to file an annual information return such as Form 990 or 990-EZ, Return of Organization Exempt From Income Tax?

- All are required to file; no exceptions.

- Any exempt organization with annual gross receipts exceeding $50,000.

- A convention or association of churches with annual gross receipts exceeding $50,000.

- Any Chamber of Commerce with annual gross receipts exceeding $50,000.

A convention or association of churches with annual gross receipts exceeding $50,000.

Organizations exempt from federal income tax under section 501(a) must file an annual information return Form 990 or 990-EZ. Notable exceptions include:

- Churches, which are not required to file Form 990, 990-EZ, or 990-N, and

- Exempt organizations with gross receipts in each tax year that normally are not more than $50,000. These organizations file Form 990-N, Electronic Notice (e-Postcard) for Tax-Exempt Organizations not Required To File Form 990 or 990-EZ.

500

Paul owns a second home at the lake. During the year, he spent three weeks (21 days) at the lake home, rented it to his daughter for three three-day weekends for a total of $220, and rented it to friends for ten weeks (70 days) at fair rental value of $300 per week. His expenses for the year include:

- Depreciation $2,000

- Insurance $100

- Mortgage interest $1,000

- Real estate taxes $2,000

- Utilities $1,000

What amount may he deduct for expenses on his Schedule E, Rental Income?

- $2,100

- $3,000

- $3,220

- $4,620

$3,220

Personal use time is a total of 30 days (21 by Paul and 9 by his daughter at less than fair market rates). The total time rented at fair rental rates is 70 days. The total days used is 100; so the allowable portion of these expenses as rental expenses is 70%. Because of the dual use of the property, Paul is unable to deduct any expenses incurred that exceed the income earned from the rental of the property ($3,220). Carry forward any amounts that are not currently deductible.

The total amount of expenses is $6,100. Of this amount, 70% would be deductible ($4,270), except that it is limited to the amount of rental income received, $3,220.