Economic Schools of thought

Supply and Demand

Trade

Producer and Consumer Surplus

Wildcard

100

What is the dominating school of thought today?

Neoclassical

100

An increase in the price causes a decrease in quantity demanded. Law of ___?

Demand

100

Consumers want to buy cheaper goods/ services from abroad

Import

100

Total surplus = ?

consumer surplus + producer surplus

100

What is Katie's Dogs name?

Emma!

200

“alternative” - catch-all for any school that differs from neoclassical

hetrodox

200

That price where the amount firms want to sell is equal to the amount people want to buy

equilibrium

200

Sellers can make more money selling abroad

Export

200

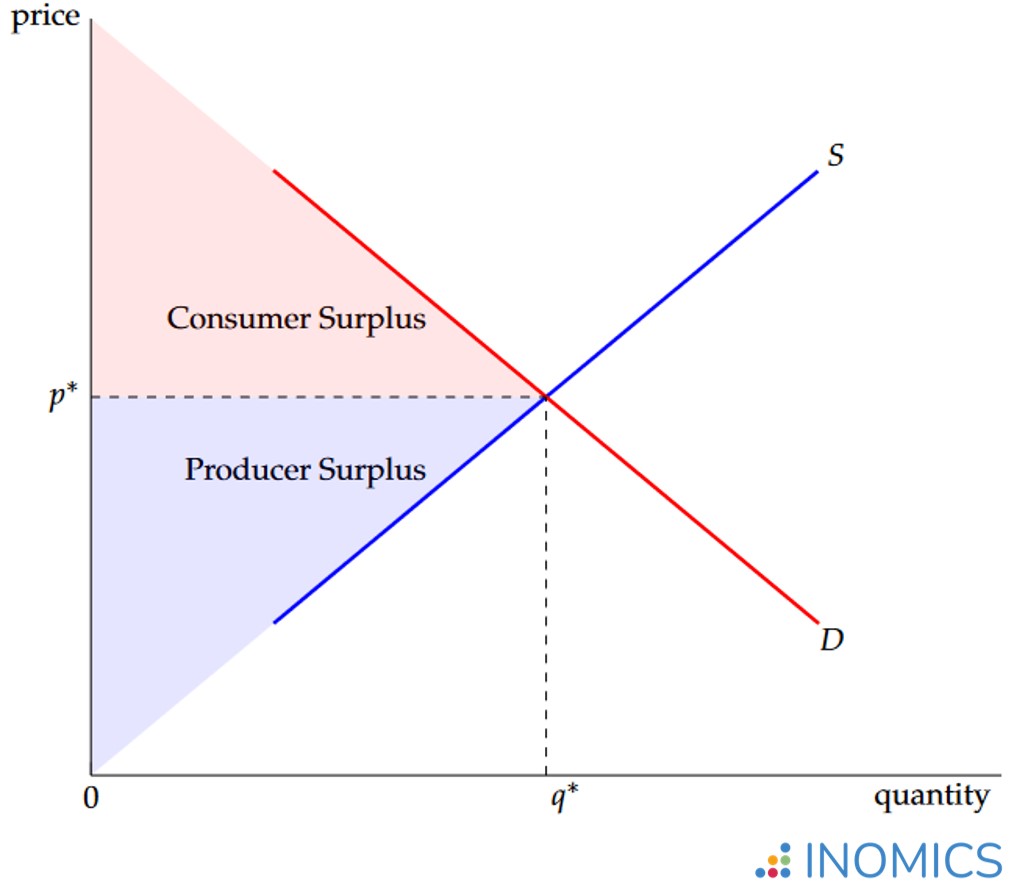

Consumer surplus =

Demand Curve - P*

200

A line/graph showing all the combinations of output possible given resources and technology

Production Possibilities Frontier

300

Neoclassical economic systems are defined by answering 3 questions, what are they?

What and how much to produce?

How to make goods and services?

Who gets these goods and services?

300

Draw a supply and demand graph on the board

Double points if you explain how you determine the change in price and quantity equilibrium when both curves shift.

:max_bytes(150000):strip_icc()/IntroductiontoSupplyandDemand3_3-389a7c4537b045ba8cf2dc28ffc57720.png)

300

This is what a good/service sells for in the world market

Price World

300

Producer Surplus

P* - Supply Curve

300

All the employees own the business together

Workers "buy in" with money to the business when they start

Each are paid a share of the profits after expenses are taken care of

Worker co ops

400

Consumers decide what is made via demand

Firms decide how to make goods and services by focusing on profit-maximizing methods

Consumers get the goods and services if they can afford it

Ultimately, it's the individuals (consumers and firms) that make decisions

Capitalism – neoclassical

400

Name the determinants of supply

Change in number of producers

change in imput costs

change in producer expectations of the future

change in technology or productivity

400

Why do nations trade?

To enjoy a higher standard of living without purchasing more scarce economic resources

400

what happens when P* moves to the right

This will transfer some ps to cs or vice versa, will also create deadweight loss

400

Producing with less opportunity cost than another firm. What do you have?

The comparative advantage

500

Typically, what most people think of as "communism" I.e. ussr

Government controls inputs

Workers made products

Government controlled profit

State capitalism – heterodox

500

Name the determinants of demand (five or six)

Change in number of consumers

change in consumer expectations of the future

change in price of a related good/substuite

chance in consumer income

change in consumer taste and preferences

exchange rate fluctuation

500

What are government tools to restrict trade?

Tariffs

Quotas

Embargos

500

Draw a producer and consumer surplus graph on the board.

500

What is Katelyn's major

Marketing and econ!