Types of Economy

Economic Terms

Europe's Economy

Geography

Trade

100

Explain Traditional economy:

based off cultural beliefs, generational, old habits & customs

100

When a country has NO trade with another country

EMBARGO

100

What type of economy does Germany have?

MIXED

100

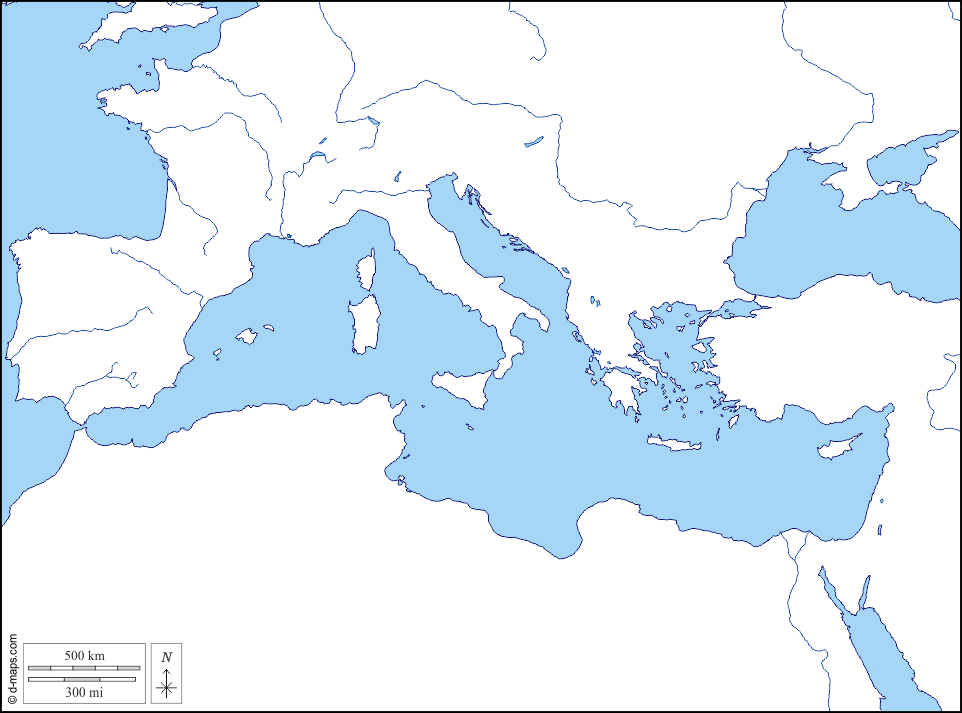

What body of water is being shown:

MEDITERRANEAN SEA

100

This type of trade barrier stops all trade between two countries, like the United States & Cuba.

EMBARGO

200

Explain how supply and demand influence what is produced in a market economy.

What is that businesses produce goods based on what consumers want and how much they’re willing to pay

200

This type of trade sets limits on the amount of items coming into the country

QUOTA

200

Most European economies have a mixed economies that lean closer to a pure ____ economy

MARKET

200

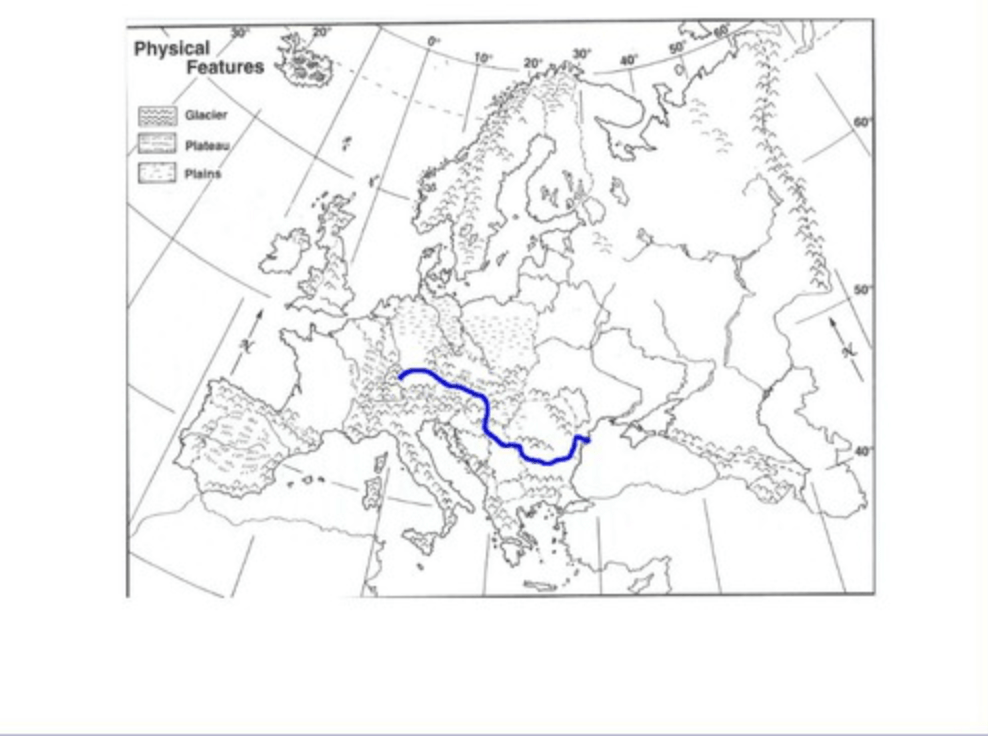

Which river is being shown:

RHINE RIVER

200

This trade barrier sets a limit on how many goods can be brought into a country

QUOTA

300

TRUE OR FALSE:

The United States has a Pure Market economy

FALSE: There's no such thing as "PURE" market or "PURE" command economy

300

A tax on trade:

TARIFF

300

Describe how the U.K.’s mixed economy combines elements of both market and command systems

What is that the U.K. has mostly market freedoms, but the government provides some services and regulates certain industries

300

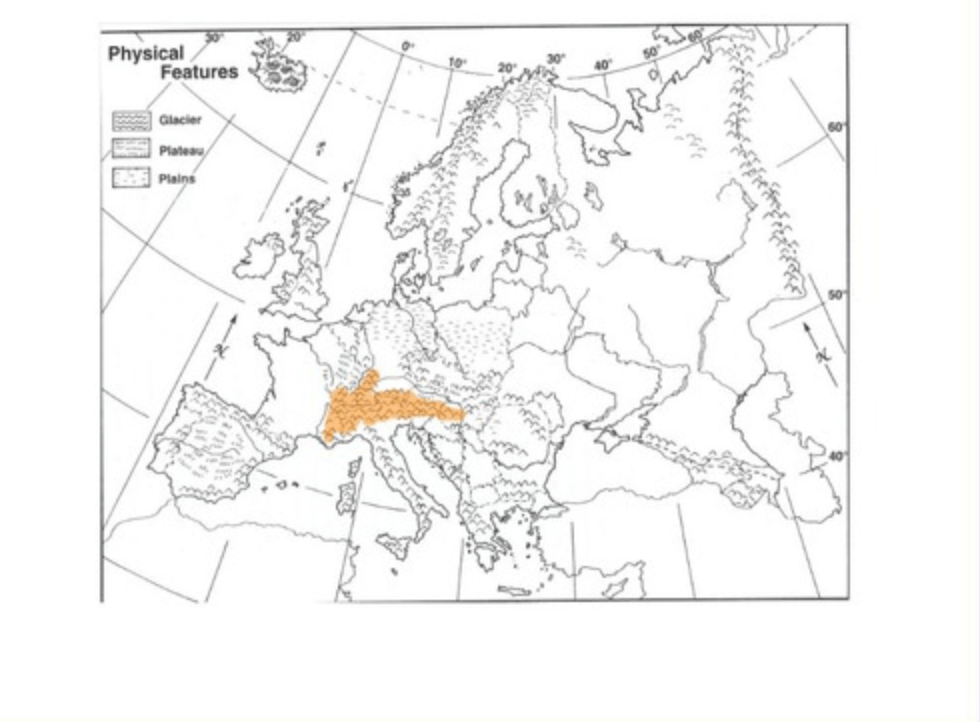

Which mountain range is being shown?

The Alps

300

Explain how SPECIALIZATION can help countries like the U.K., Germany, and Russia increase trade with other nations.

Specialization helps countries focus on producing goods they make best or most efficiently. By focusing on their strengths, these countries can trade with others for the goods they don't produce

400

What are the 3 basic economic questions?

1. What to produce

2. How to produce

3. For whom to produce for

400

Explain how a tariff on imported goods can affect the price of those goods for consumers.

tariffs make imported goods more expensive for consumers

400

A local bakery decides to make more chocolate cupcakes because customers have been buying them faster than other flavors. The bakery lowers the price of vanilla cupcakes to encourage sales. Which type of economy is being described, and why do businesses make these kinds of decisions?

What is a market economy, where businesses respond to supply & demand, and consumer choices to decide what and how much to produce

400

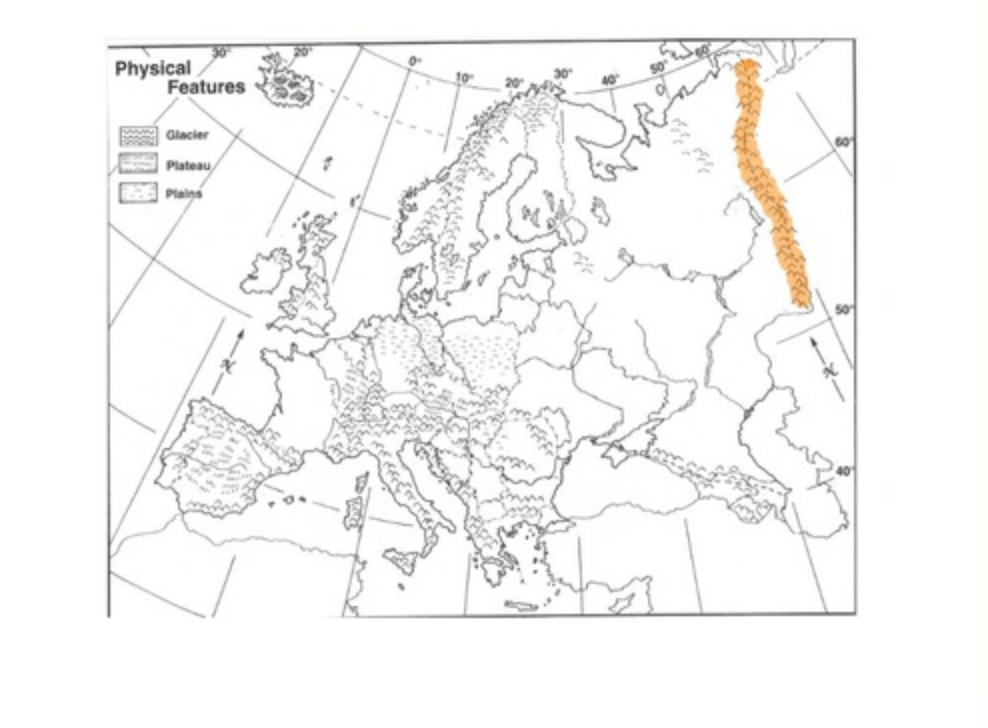

Which mountain range is shown:

The Ural Mountains

400

Describe how investing in CAPITAL GOODS, like machines and factories, can help economies grow

It helps economies grow because it makes production faster and more efficient. When businesses can produce more goods in less time, they can sell more products

500

Compare how decisions about what to produce are made in a command economy versus a market economy.

In a command economy the government makes the decisions, but in a market economy individuals and businesses decide

500

In a traditional economy, people often follow the same jobs and roles as their parents and grandparents. Explain how this way of life can both help and limit a community’s ability to adapt to change

it helps keep traditions and skills alive, but makes it hard to adopt new technology or respond to outside changes

500

In a small village, families grow the same crops their parents grew, make their own clothes by hand, and trade goods with neighbors instead of using money. They rarely change how they do things, even when new technology arrives. What type of economy is being described?

Traditional economy

500

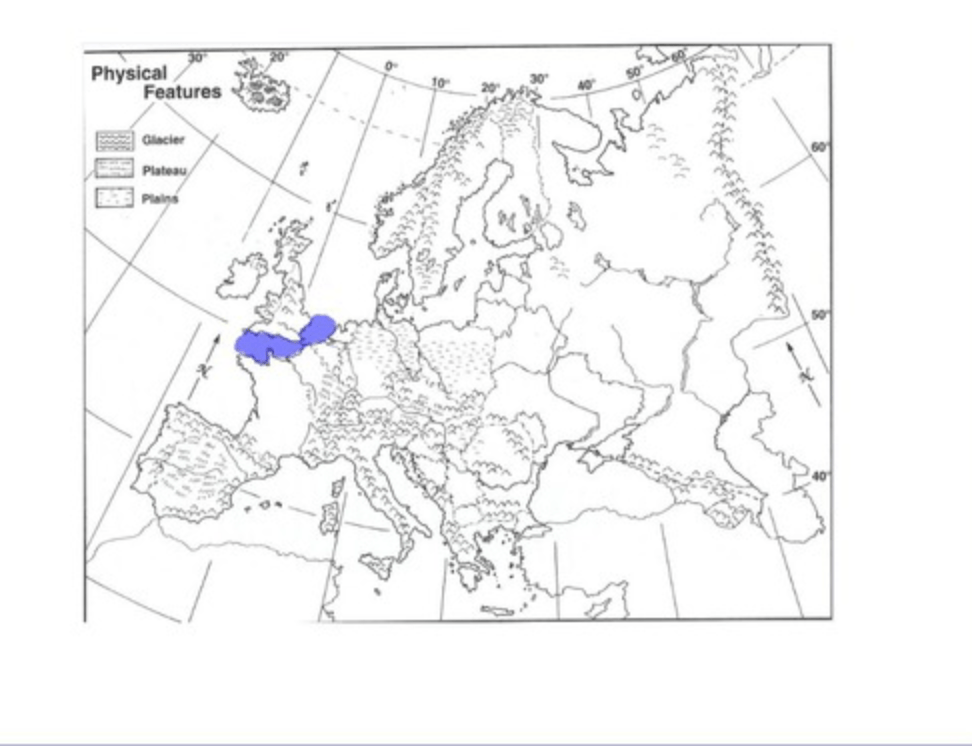

What is this physical feature and how has this body of water influenced trade and travel?

English Channel; natural trade barrier effecting shipping and traveling from U.K. to mainland Europe. Allows items to be shipped quickly and travel made easier

500

Explain how investing in HUMAN CAPITAL, such as education and training, can improve a country's GDP (Gross Domestic Product)

Investing in human capital through education and training helps workers gain skills and knowledge. Skilled workers can do their jobs and produce higher-quality goods and services, which improves a nations GDP.