Graphs

Production

Perfect Competition

Long Run

Short Run

100

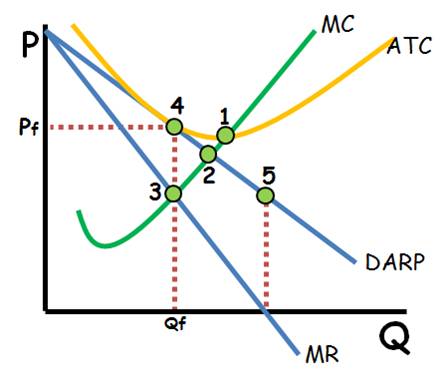

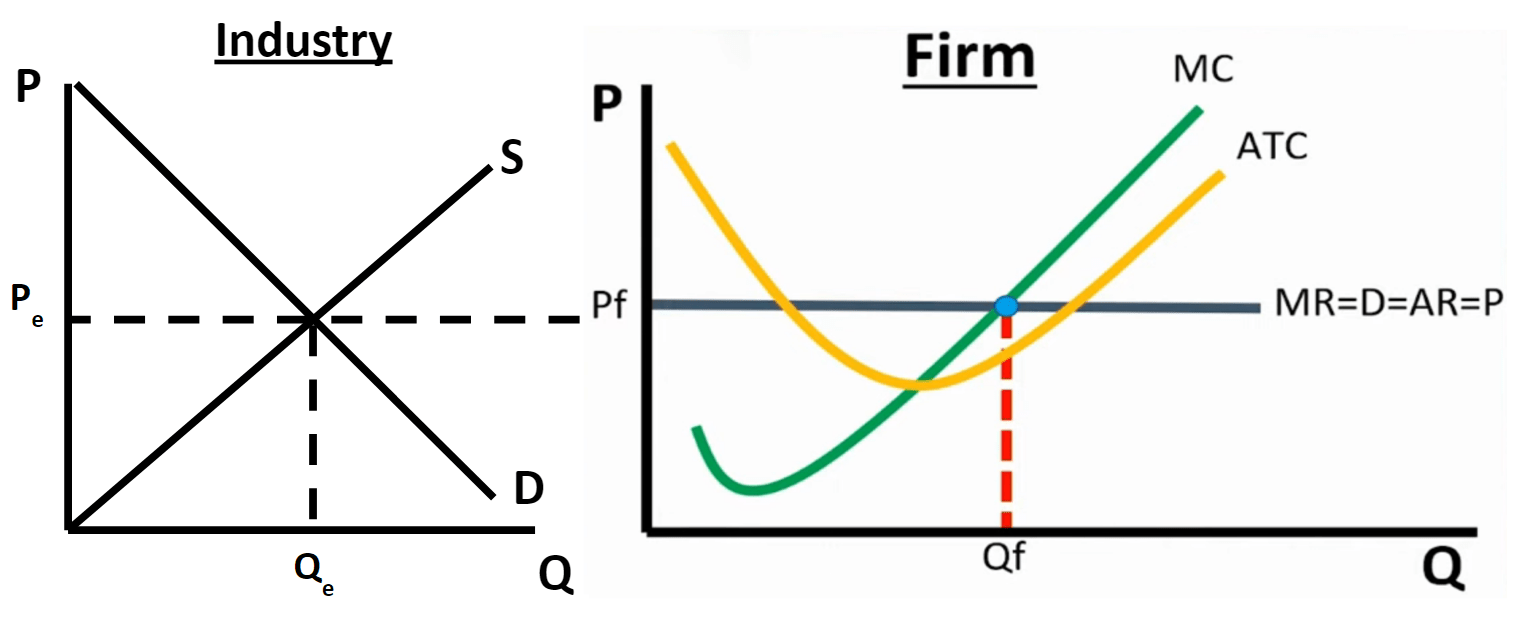

The Profit Maximizing Quantity AND Price

What is:

Quantity = 3 or Qf

Price = 4 or Pf

100

What is the Profit - Maximizing Point?

MR = MC

100

What kind of firms are perfectly competitive firms?

a) Wage Takers

b) Price Takers

c) Price Makers

B!

100

Define: Long Run

A period of time in which all resources can change

100

Define: Short Run

A period of time in which at least one resource is fixed

200

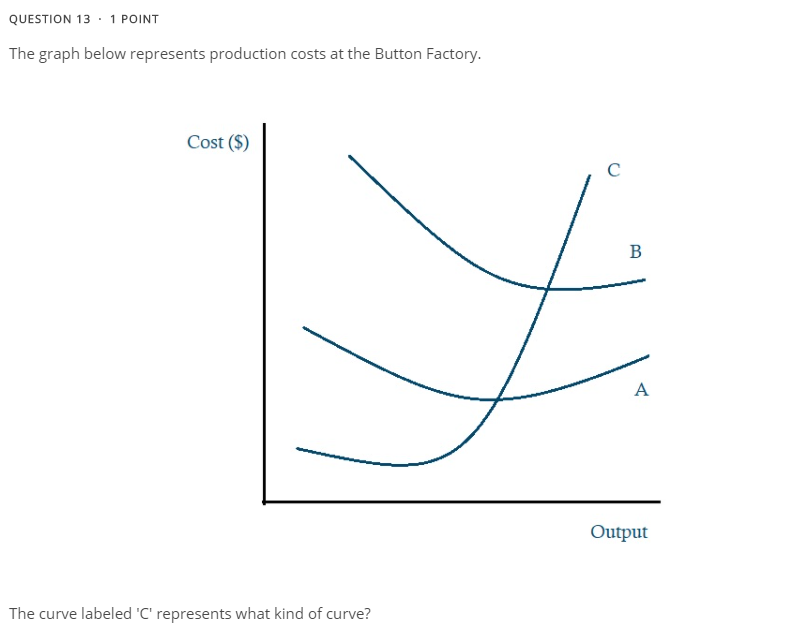

Name the cost curves from A - C

What is

A = Average Variable Cost

B = Average Total Cost

C = Marginal Cost

200

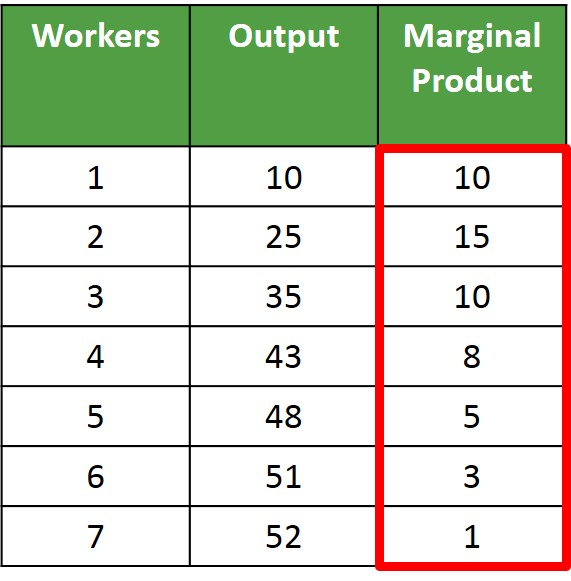

At what unit does Diminishing Marginal Returns set in?

At the 3rd worker

200

CerealCo is one of many producers that make corn flakes in a perfectly competitive market. If they sell their corn flakes at $6/box, what price does Wheat Ltd. have to sell their corn flakes at?

Wheat Ltd. must also sell at $6

200

What type of profit do perfectly competitive firms make in the long run?

Zero Economic Profit or Normal Profit

200

Short run marginal costs eventually increase because of the effects of...

Diminishing Marginal Products

300

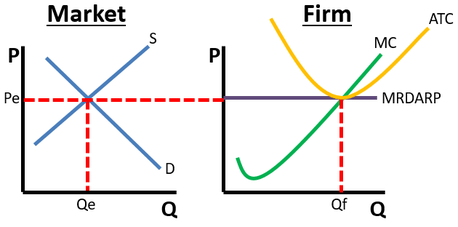

What type of market is this

Perfect Competition Market

300

Define: Diminishing Marginal Returns

As you add variable resources to fixed resources, the additional output will eventually decrease

300

The profit maximizing quantity

MR = MC

300

Which of the following must be true of the long run?

A) All factors of production are fixed

B) Factors of production are not considered

C) At least one factor of production is fixed

D) All factors of production are variable

D!

300

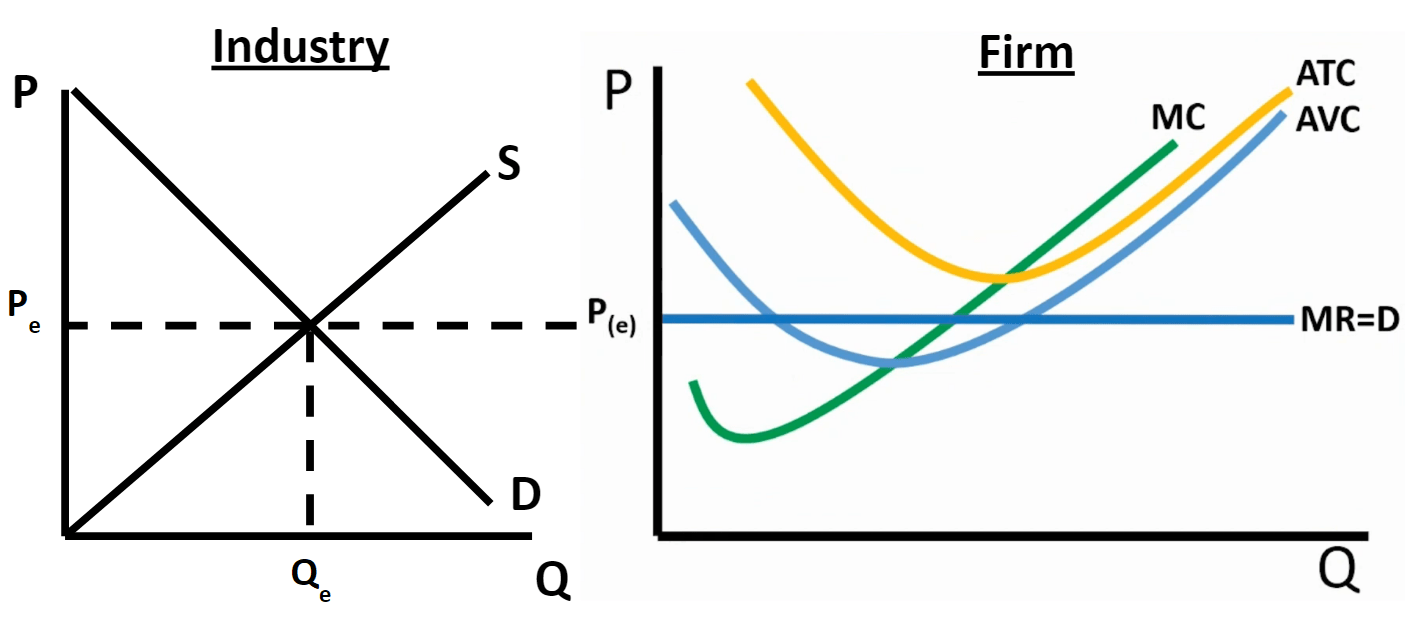

A profit-maximizing firm will shut down in the short run any time the firm’s total revenue is less than its:

Total Variable Cost

400

Draw a perfectly competitive firm producing with a positive profit.

400

A firm expands its fixed resources and its overall costs of production go up. It is experiencing...

Negative returns to scale

400

The elasticity of a perfectly competitive demand curve is:

Perfectly Elastic

400

What's must be true if a firm is in economies of scale?

A) The LRATC decreases as output increases

B) The LRATC increases as output increases

C) The LRATC shifts right, towards the output

D) The LRATC shifts left, away from the output

A!

400

Assume that a profit-maximizing, perfectly competitive firm has economic losses in the short run. Why would a firm continue to operate at a negative profit?

The firm is covering its variable costs but failing to cover all of its fixed costs

500

Draw a Perfectly Competitive firm producing at a loss but not shutting down.

500

Tony opens up a hot chocolate stand for two hours. He spends $10 for ingredients and sells $60 worth of tasty beverages. In the same two hours, he could have provided Uber services and earned $40. Tony's accounting profit is ____ and an economic profit of ____.

Accounting Profit: $50

Economic Profit: $10

500

At Price G, the area of which rectangle represents total revenue for the profit-maximizing competitor?

0GKC

500

Assume that Mr. Prince's firm is one of many that produce AP Micro Topic worksheets in a perfectly competitive industry which is currently in long-run equilibrium. If the current price for worksheets is $.50, and demand is increasing, how will the price change in the SR and LR?

A) SR= greater than $.50 | LR= greater than $.50

B) SR = greater than $.50 | LR = equal to $.50

C) SR = greater than $.50 | LR = less than $.50

B!

500

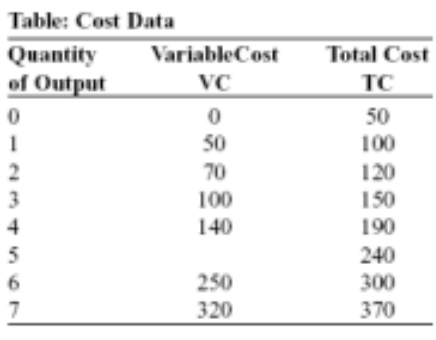

What is the value of the variable cost for this firm when the firm is producing five units of output?

$190